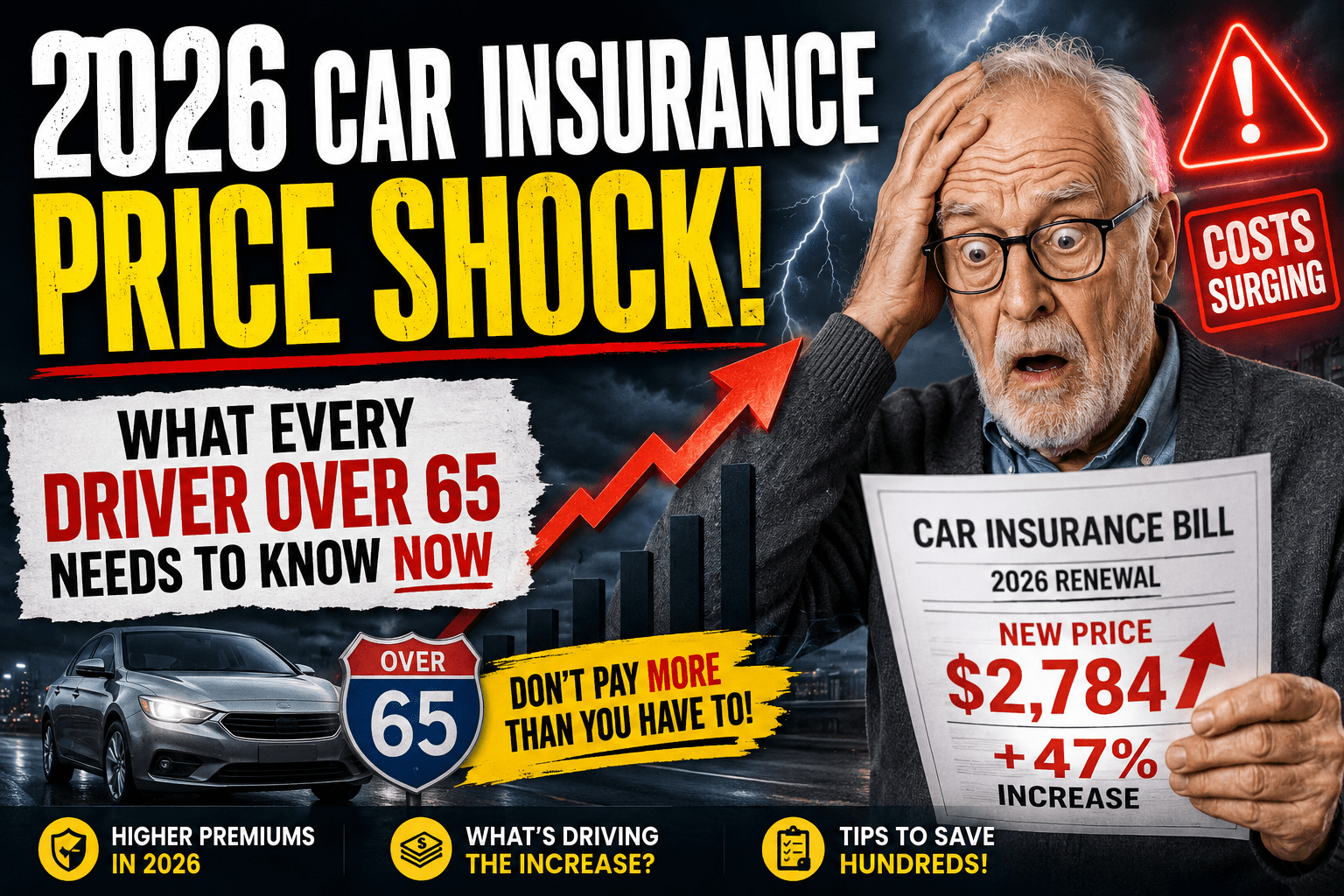

2026 Car Insurance Price Shock: What Every Driver Over 65 Needs to Know Now

If your premium renewal notice made you do a double-take this year, you’re not imagining things. Rates for senior drivers have climbed faster in 2026 than at any point in the past decade — and the reasons behind it are more complicated than insurers want you to know.

Short Summary

In 2026, car insurance for elderly drivers has hit record highs — with drivers over 65 seeing average premium increases of 18–31% compared to 2024. Factors include rising repair costs, litigation funding, climate disasters, and age-based actuarial models that now flag drivers as higher-risk earlier than ever. The good news: smart comparison shopping, low-mileage discounts, defensive driving courses, and bundling strategies can still save you hundreds of dollars per year. This guide breaks down exactly what’s happening, who’s getting hit hardest, and what to do about it right now.

TL;DR – Quick Summary

- Premiums for drivers 65+ are up 18–31% in 2026 vs. two years ago.

- Drivers over 75 and especially over 80 are facing the steepest increases — some exceeding 40%.

- Florida, California, and Texas are the hardest-hit states for senior drivers.

- The best companies for seniors right now are USAA (if eligible), The Hartford/AARP, and Geico.

- Low-mileage discounts, bundling, and telematics are the three biggest money-savers available today.

- Shopping quotes every 12 months is no longer optional — it’s the single most effective way to avoid overpaying.

Why Is Car Insurance Suddenly So Expensive for Drivers Over 65 in 2026?

I remember the exact moment I realized something had changed. My neighbor Margaret — 68 years old, spotless driving record, drives maybe 5,000 miles a year — called me in genuine shock after opening her renewal letter. Her annual premium had jumped from $1,340 to $1,890. No accidents. No tickets. No claims. Just her birthday getting closer to 70.

That wasn’t a fluke. Across the country, car insurance for senior drivers has become one of the fastest-rising household expenses of 2026. And while it feels personal — like the insurance company has it out for you specifically — the truth is, a perfect storm of economic and structural forces has collided in a way that’s hurting older drivers more than anyone else.

The core issue is this: insurance companies are playing catch-up. For years, they underpriced risk — and now they’re correcting aggressively, using actuarial models that increasingly single out older age brackets as higher-cost customers. The result is a rate shock that’s hitting seniors who’ve been loyal, careful drivers for decades.

How Much More Will Seniors Pay for Car Insurance in 2026?

Let’s be blunt about the numbers, because sugarcoating them doesn’t help anyone. The average driver between 65 and 69 is now paying roughly $1,780–$2,100 per year for full coverage in 2026 — up from $1,480–$1,720 just two years ago. Drivers between 70 and 74 are averaging $2,100–$2,600. And once you cross 75, many drivers are being quoted $2,700 or more — even with clean records.

That’s not a gentle trend. That’s a structural shift in how insurers price auto insurance for elderly drivers.

| Age Bracket | Avg. Premium 2024 | Avg. Premium 2026 | % Increase |

|---|---|---|---|

| Ages 65–69 | $1,600 | $1,940 | +21% |

| Ages 70–74 | $1,850 | $2,350 | +27% |

| Ages 75–79 | $2,100 | $2,730 | +30% |

| Ages 80+ | $2,500 | $3,450 | +38% |

Note: Figures represent national averages for full coverage (liability + collision + comprehensive). Rates vary significantly by state, driving history, and vehicle type.

What Is Causing the 2026 Car Insurance Price Shock for Seniors?

This isn’t about one thing. It’s about five or six things hitting simultaneously — and older drivers absorbing the heaviest impact because of how insurers build their models.

1. Vehicle Repair Costs Have Gone Through the Roof

Modern vehicles — even “ordinary” ones — are now packed with sensors, cameras, and advanced driver-assistance systems. A minor fender bender that would’ve cost $800 to fix five years ago now runs $2,500 because the bumper has three sensors, a camera, and requires dealer calibration. Insurers are paying these bills, and they’re passing those costs on — especially to age brackets statistically more involved in minor collisions.

2. Medical Cost Inflation Is Spiraling

When someone is injured in an accident, personal injury protection and bodily injury liability claims have exploded in cost. Hospital stays, physical therapy, and post-accident care are dramatically more expensive than they were even three years ago. Older drivers — who are statistically more likely to require extended medical care after a collision, even when they aren’t at fault — get flagged as higher-liability customers.

3. Climate-Related Claims Are Adding Up

Floods, hailstorms, wildfires — the frequency of comprehensive claims has jumped sharply. In states like Florida, Texas, and California, insurers have taken massive losses. Those losses get distributed across all policyholders, but age-based risk models amplify the impact on seniors.

4. Litigation Funding Is a Silent Driver

Third-party litigation funding — where investors bankroll lawsuits against insurers in exchange for a cut of the settlement — has exploded. This inflates claim settlements and legal costs, which insurers recoup through higher premiums. It’s a factor most seniors never hear about, but it’s very real.

5. Reinsurance Costs Have Skyrocketed

Insurance companies buy their own insurance — called reinsurance — to cover catastrophic losses. Reinsurance rates have risen 30–50% in recent years, and that cost cascades directly into your premium renewal letter.

Why Are Insurance Companies Raising Rates So Aggressively for Elderly Drivers?

Insurance is a numbers game, and the numbers for older drivers have shifted. Actuarial data — the statistical backbone of every premium calculation — shows that accident rates begin climbing again after age 70, largely due to factors like slower reaction times, vision changes, and certain medications. I don’t say this to be harsh; it’s simply what the data shows, and insurers are leaning into it harder than ever in 2026.

What’s different now versus five years ago is how granularly they’re slicing that data. It’s no longer just “65+ is a higher-risk tier.” Companies are now running models that differentiate meaningfully between a 67-year-old and a 72-year-old, and between a 72-year-old and a 78-year-old. Each of those brackets carries a noticeably different premium in 2026.

The frustrating part — and I’ve heard this from dozens of seniors — is that individual driving quality is getting lost in the statistical noise. A 74-year-old who drives carefully, never speeds, and has logged zero claims in 12 years still gets lumped into a high-rate bracket because of what the average 74-year-old costs insurers.

Is Age 65+ the New High-Risk Category for Auto Insurance?

Not exactly — but the goalposts have moved. A few years ago, most insurers started flagging risk more meaningfully at age 70 or 75. In 2026, some companies are now building rate increases into their models starting at age 65. That’s a significant shift, and it means auto insurance for elderly drivers is becoming a distinctly different product category than it was even three years ago.

The silver lining — if you can call it that — is that the spread between different insurers has also widened. Because each company applies its own actuarial models, the difference between the cheapest and most expensive quote for the same 68-year-old driver can be $600–$900 per year. That gap is your opportunity.

How Much Does Car Insurance Cost for Seniors Over 65 in 2026?

The range is wide, which is exactly why comparing car insurance quotes for seniors matters so much right now. Your specific rate depends on your state, your driving record, the vehicle you drive, how many miles you log annually, and which company you’re with.

That said, here are realistic ballpark figures for 2026 based on national averages. For more granular detail specifically on quote ranges by state and coverage type, I’d recommend also checking out our deep-dive on average car insurance quotes for elderly drivers in 2026.

| Age | Low-End Estimate | Mid-Range | High-End |

|---|---|---|---|

| Age 65 | $118/mo | $148/mo | $195/mo |

| Age 70 | $135/mo | $175/mo | $228/mo |

| Age 75 | $158/mo | $207/mo | $265/mo |

| Age 80+ | $195/mo | $258/mo | $340/mo |

What Is the Average Car Insurance Cost for 70, 75, and Over 80 Drivers Right Now?

This is the question I get asked most often, and the honest answer is: it depends enormously on where you live and which company you’re with. But let me give you the clearest picture I can.

A 70-year-old driver with a clean record in a mid-tier state (think Ohio, Virginia, or Michigan) can reasonably expect to pay $1,800–$2,400 per year for full coverage in 2026. Push that to age 75 and you’re looking at $2,200–$2,900. For drivers over 80, see our dedicated guide on over 80 car insurance costs in 2026 — because the situation for that age bracket has some unique considerations worth exploring in detail.

The key thing I want you to take away from these numbers: the range within each age bracket is enormous. The difference between the best and worst quote for the same 72-year-old driver can be $700–$1,000 per year. That’s the gap comparison shopping closes.

Which Age Group Is Seeing the Biggest Insurance Rate Increases in 2026?

The steepest increases are concentrated in the 75–84 age bracket. This group has absorbed disproportionate rate hikes compared to both younger seniors (65–74) and drivers over 85 (who are often already in specialty markets). If you’re in your late 70s and you’ve noticed your rate climbing two or three years in a row, you’re in the bull’s-eye of this trend.

Drivers in the 70–74 range are seeing significant increases too — particularly if they’ve had any claims in the past three years. For a dedicated look at over 70 car insurance rates in 2026, I’ve put together a focused breakdown of what that age group is specifically facing.

Why Do Insurance Companies Charge Elderly Drivers More in 2026?

Let me be direct about this, because you deserve a straight answer rather than corporate-speak. Insurers charge car insurance for elderly drivers at higher rates for a straightforward reason: their internal data shows that claim costs rise with age, particularly for liability and medical payments.

Specifically, older drivers are more likely to:

- Be injured more seriously in accidents of equivalent severity (higher medical cost per claim)

- Require longer recovery periods, inflating medical payments coverage costs

- Have slower reaction times that statistically increase at-fault accident frequency after age 75

- Drive older vehicles or vehicles not equipped with modern safety technology

None of this means you’re a bad driver. It means you’re being priced based on group statistics rather than your individual record — and that’s a distinction worth fighting back against through smart shopping and discount stacking.

How Does Your Health and Driving Habits Affect Car Insurance Quotes for Seniors?

Here’s something not enough people talk about: your behaviors have a bigger impact on your premium than your age in many cases — if you use the right tools to demonstrate them.

Telematics programs (also called usage-based insurance) track how you actually drive — braking behavior, speed consistency, time of day, mileage. If you drive carefully and infrequently, these programs can reduce your premium by 10–25%. For seniors who drive mostly during daylight hours in familiar areas, telematics is often the fastest route to a lower rate. While health conditions themselves aren’t directly disclosed to insurers (HIPAA protects you), medications that affect alertness are something drivers should be mindful of for safety reasons, which indirectly protects your driving record.

My experience: I’ve seen seniors dismiss telematics because they’re worried about being “spied on.” In most cases, that worry costs them $200–$400 a year for no good reason. If you drive carefully — and most seniors I know do — telematics is almost always worth trying. You can opt out if the program ends up working against you.

Is It Getting Harder for Drivers Over 70 to Even Get Car Insurance?

In some cases, yes — and this is a trend I’m watching closely. A handful of regional insurers have quietly tightened their eligibility criteria for drivers over 75, particularly those with even minor claims history. In a few states, drivers over 80 are being declined by standard carriers and redirected to surplus lines or state-assigned risk pools, which carry significantly higher premiums.

This isn’t a crisis for most seniors yet, but it’s the direction the market is trending. The response is to stay proactive: shop early (before your renewal date), maintain a clean record, and consider working with an independent agent who has access to multiple carriers — including specialty markets for older drivers. For a full analysis of this access problem, check out our separate piece: Is car insurance for elderly drivers getting harder to find in 2026?

What Are the Best Car Insurance Companies for Senior Citizens in 2026?

Not all insurers treat older drivers the same way. Some genuinely compete for senior customers with favorable rating models and age-specific discounts. Others quietly penalize age more harshly. Here’s my honest breakdown of the major players — and then we’ll look at real-world comparisons.

For detailed reviews of each, check our companion articles: best car insurance for senior citizens in 2026 and best auto insurance for senior citizens — 2026 comparison.

| Company | Best For | Senior Discounts | Age 65+ Rating | Age 75+ Rating |

|---|---|---|---|---|

| USAA | Military veterans/families | Excellent | ★★★★★ | ★★★★★ |

| The Hartford / AARP | Seniors 50+ / AARP members | Excellent | ★★★★★ | ★★★★☆ |

| Geico | Low base rates / online ease | Good | ★★★★☆ | ★★★☆☆ |

| Progressive | Low-mileage / telematics | Good | ★★★★☆ | ★★★☆☆ |

| State Farm | Agent-based service / bundling | Moderate | ★★★☆☆ | ★★★☆☆ |

| Nationwide | Bundling deals / SmartRide | Moderate | ★★★☆☆ | ★★★☆☆ |

Which Insurance Companies Offer the Cheapest Car Insurance for Elderly Drivers?

Based on quote comparisons across multiple states in 2026, USAA consistently delivers the lowest rates for eligible seniors — often 15–25% below the market average. For those without military affiliation, Geico and The Hartford frequently emerge as the most competitive options for drivers in the 65–74 range. Progressive tends to excel for seniors who drive fewer than 8,000 miles per year and opt into their Snapshot telematics program.

The critical thing to understand: “cheapest” isn’t static. The cheapest company for a 68-year-old in Arizona might be completely different from the cheapest company for a 68-year-old in Michigan. This is why real quotes — not generic estimates — are the only reliable guide.

How Do AARP, Hartford, USAA, and Progressive Compare for Seniors Over 65?

AARP / The Hartford is purpose-built for older drivers and offers features that no general-market insurer matches: a lifetime renewability guarantee (they won’t drop you for age alone), a RecoverCare benefit (helps pay for services you can’t perform while recovering from an accident), and disappearing deductibles for long-term customers. For seniors who value stability and specialized service over the absolute lowest premium, this is often my top recommendation.

USAA is unbeatable on price for veterans and military families — but you must be eligible. If you or your spouse served, this should be your first call, no question.

Progressive’s Snapshot program has quietly become one of the best tools for seniors who drive carefully and infrequently. If your annual mileage is under 8,000, the telematics discount alone can offset a meaningful chunk of your rate increase.

My recommendation: Get a quote from all three. Even if you’ve been loyal to one company for years, the market has shifted enough in 2026 that brand loyalty without comparison shopping is just leaving money on the table.

How Can Drivers Over 65 Get Lower Car Insurance Quotes in 2026?

This is the section I most want you to bookmark. Because despite everything I’ve described above, there are real, actionable levers you can pull. The increase doesn’t have to be your reality.

Step-by-Step: How to Lower Your Senior Car Insurance Rate in 2026

Know your exact coverage levels, deductibles, and current annual premium before you start shopping. You can’t compare intelligently without a baseline.

Use online comparison tools, then call USAA and The Hartford directly — because those two often quote better by phone for seniors. Don’t just renew automatically.

Agents don’t always volunteer them. Ask directly: “What senior discounts do you offer? What’s the discount for defensive driving? Low mileage? Bundling?” See our full guide to senior citizen discount car insurance for the complete list.

If you drive under 7,500 miles a year — which many retired seniors do — you may qualify for 10–20% off. Some insurers offer per-mile pricing programs that can save even more.

AARP’s Smart Driver course and AAA’s Road Wise Driver program are both accepted by most major insurers for discounts of 5–15%. They’re online, inexpensive, and take about 6–8 hours.

This single move saves most seniors $150–$350 per year. If your home and auto are currently with different companies, recalculate the combined cost with one insurer — the math often surprises people.

Raising your deductible from $500 to $1,000 typically reduces your premium by 8–12%. Only do this if you could comfortably cover the higher deductible out of pocket in an emergency.

What Senior Car Insurance Discounts Are Still Available This Year?

Despite the rate increases, the discount landscape for seniors hasn’t evaporated — it’s just become more important to actively claim every discount you qualify for. Here’s what’s still on the table in 2026.

For the complete deep-dive on which discounts are still working and which have been quietly reduced, check our dedicated guide: discount car insurance for seniors — how to save hundreds in 2026. Here’s the quick version:

- Defensive Driving Discount: 5–15% at most major insurers (requires course completion)

- Low-Mileage Discount: 10–20% if under 7,500 miles/year

- Bundle Discount: 8–18% when combining home and auto

- Loyalty Discount: 3–10% for multi-year customers (check if your loyalty discount is still beating competitor quotes)

- Telematics Discount: 10–25% for safe driving as measured by a usage-based program

- Pay-in-Full Discount: 5–8% for paying your annual premium upfront

- Paperless Billing Discount: $5–15/year (small but free)

Does Taking a Defensive Driving Course Still Save Money for Seniors?

Yes — and this is one of the most consistently underused tools in a senior driver’s toolkit. Most major insurers still offer a meaningful discount (5–15%) for completing an approved defensive driving course. AARP’s Smart Driver course costs about $17–$20 online and qualifies you for discounts at The Hartford, Allstate, State Farm, and others for three years.

💡 If I Were in Your Shoes…

I’d take the online defensive driving course before getting new quotes — not after. That way, you can claim the discount immediately when insurers ask if you’ve completed an approved course. A $20 investment that earns you $100–$200 off your annual premium is one of the best ROI moves you can make this year.

How Much Can Low-Mileage Drivers Over 65 Save on Auto Insurance?

This is bigger than most people realize. The average retired senior drives roughly 6,000–8,000 miles per year — well below the national average of 14,000–15,000. If you’re in that range, you’re statistically much less likely to file a claim, and some insurers will price that accordingly.

Through low-mileage discounts or pay-per-mile programs (like Nationwide’s SmartMiles or Allstate’s Milewise), a senior driving 5,000 miles per year might save $250–$450 annually compared to a standard policy. The catch: you need to be willing to report your mileage honestly and, in some cases, use a tracking device. For the math on whether this works for your situation, see our piece on cheap car insurance for seniors over 65.

Is Bundling Home and Auto Insurance Worth It for Senior Citizens?

In the vast majority of cases — yes. Bundling consistently delivers the largest single-move discount available to most seniors, typically reducing your total insurance bill (home + auto combined) by 8–18%.

The scenario where bundling doesn’t make sense: when one insurer has a dramatically better deal on your home coverage and another on your auto, and the bundling discount doesn’t bridge that gap. That’s why the right move is to get bundled quotes from two or three companies and compare them against your current split-policy costs.

My advice: Call The Hartford, State Farm, and Allstate for bundled quotes. Present your current home and auto costs to each one. Let them compete. In my experience, at least one will come in lower than what you’re paying now — sometimes by $300–$500 a year.

Should You Switch Insurance Companies If You’re Over 65?

Brand loyalty is a beautiful thing — until it costs you $600 a year. The hard truth is that in 2026, the insurance market has changed enough that many seniors who’ve been with the same company for 10 or 15 years are now significantly overpaying. Insurers don’t typically reward longevity the way they once did, and new-customer promotions often beat loyalty discounts by a wide margin.

That said, switching has a real cost: you may lose a loyalty discount, you’ll need to re-establish your claims history with a new provider, and some perks (like The Hartford’s disappearing deductible) require years of consistent coverage to fully vest. The right answer depends on the size of the savings gap. If a competitor is more than $200/year cheaper with equivalent coverage — switch. If it’s $80 — probably not worth the friction. Use that number as your personal threshold.

What Should You Do If Your Car Insurance Premium Increased Dramatically in 2026?

First: don’t panic, and don’t just accept it. Here’s the action plan.

- Call your current insurer and ask for a review. Sometimes increases can be partially reversed, especially if you’ve had no claims.

- Ask specifically what caused the increase. Was it a claim? An actuarial age adjustment? A regional rate filing? The answer tells you how to respond.

- Get three to five comparison quotes before your renewal date. Start shopping 45–60 days before your renewal — that gives you time to switch without a coverage gap.

- Stack every applicable discount with each new quote you receive.

- Consider an independent agent. Unlike captive agents who sell one company’s products, independent agents can shop multiple carriers simultaneously — including regional and specialty insurers that don’t advertise heavily.

Is It Better to Drop Full Coverage After Age 70?

This depends almost entirely on your vehicle’s value. The general rule of thumb is: if your car is worth less than 10 times your annual collision/comprehensive premium, dropping to liability-only may make financial sense.

Example: if collision and comprehensive coverage costs you $700/year and your car is worth $5,000, you’re paying 14% of the car’s value annually for coverage with a $500 deductible — netting you only $4,500 in the worst case. That math doesn’t hold up well.

Important caveat: If you’re still making payments on your vehicle, your lender requires full coverage. And if you couldn’t easily replace your car with cash in the event of a total loss, keep the full coverage. The right move is situation-specific — but it’s worth doing the math rather than assuming you need what you’ve always had.

Which States Are Hit Hardest by the 2026 Car Insurance Price Shock for Seniors?

Not all states are feeling the same level of pain. State-specific factors — insurance regulation, litigation environment, weather patterns, and population density — create enormous geographic variation in what seniors pay.

| State | Avg. Annual Premium (Age 70) | 2024–2026 Change | Key Driver |

|---|---|---|---|

| Florida | $3,200+ | +41% | Litigation + storms |

| California | $2,900+ | +35% | Wildfires + regulation |

| Texas | $2,700+ | +33% | Hail + litigation |

| Michigan | $2,600+ | +28% | No-fault system costs |

| Vermont | $1,280 | +14% | Low density / low claims |

| Maine | $1,310 | +15% | Low litigation rates |

| Idaho | $1,380 | +16% | Rural + low-risk profile |

How Bad Is the Situation for Senior Drivers in Florida, California, and Texas?

Florida is in a category of its own. It has the highest concentration of senior drivers in the country, one of the most lawsuit-permissive legal environments, and recurring hurricane and flood damage. Senior drivers in Florida are paying 40%+ more than they were two years ago in many cases, and several insurers have restricted new policies in the state entirely.

California is complicated by its unique regulatory environment — the state requires prior approval for rate increases, which caused a years-long backlog. Now that regulators have approved increases, carriers are making up for lost time. The result is sharp increases landing all at once for California seniors in 2025–2026.

Texas is hit hard by severe weather — hail events in particular — and has one of the highest rates of litigation-funded lawsuits related to auto accidents. For seniors in these three states especially, comparison shopping isn’t optional — it’s survival.

What Should Every Driver Over 65 Do Right Now About Their Car Insurance?

Your 2026 Action Checklist

- ☑ Review your current policy — know exactly what you’re paying and for what coverage

- ☑ Check your annual mileage — if under 8,000 miles, you likely qualify for a discount

- ☑ Complete a defensive driving course (AARP or AAA)

- ☑ Get quotes from at least 4 insurers before your next renewal

- ☑ Ask each insurer about every available senior discount

- ☑ Get a bundled home+auto quote from any insurer you’re seriously considering

- ☑ Evaluate whether your current coverage level still makes sense for your vehicle’s value

- ☑ Set a calendar reminder to repeat this process every 12 months

How to Get the Best Car Insurance Quotes for Seniors in Minutes

The process of getting real, usable quotes has never been faster — but there’s a right way and a wrong way to do it.

The wrong way: entering your information into one of those aggregator sites that sell your data to a dozen insurance agents, then spending a week fielding calls you didn’t ask for.

The right way:

- Have your current policy, vehicle information (VIN, year, make, model), and driver’s license ready.

- Go directly to USAA, The Hartford, Geico, and Progressive’s own websites for quotes — or call them directly for the 65+ experience.

- Use a reputable comparison tool (not a lead-gen aggregator) for mid-tier regional insurers.

- Compare apples to apples — same coverage limits and deductibles across every quote.

- Take the best offer back to your current insurer and ask if they’ll match it. Sometimes they will.

For more detail on finding cheap rates specifically, check our companion guide: how to get cheap car insurance for seniors over 65 in 2026.

Frequently Asked Questions

Is it legal for insurance companies to charge more based on age?

Yes — age is a legally permitted rating factor in all U.S. states. Unlike health insurance under the ACA, auto insurance is not required to ignore age. Insurers use it as an actuarial variable, though some states limit how aggressively it can be applied.

Can an insurance company drop me just because I turned 70?

Generally, no — most states prohibit non-renewal of a policy based solely on age. However, insurers can raise your rates, require a driving evaluation, or non-renew for other legitimate reasons (accident history, claims record). The Hartford/AARP has a specific “no non-renewal due to age” guarantee that most insurers do not match.

Does my Medicare or supplemental health insurance affect my car insurance cost?

Not directly — insurers don’t access your health insurance information. However, your Medicare coverage can affect how medical payments (MedPay) claims interact with your auto policy. Speak with your agent about how your health coverage coordinates with your auto insurance to make sure you’re not paying for duplicate coverage.

What’s the best car insurance company for a driver over 80?

The Hartford/AARP consistently ranks highest for drivers over 80 due to its age-neutral renewal guarantee and specialized senior benefits. USAA is superior on price for eligible veterans. For a full breakdown specific to this age group, see our article on over 80 car insurance in 2026.

Should I use an insurance broker or go direct for senior car insurance?

An independent broker (not a captive agent) can be particularly valuable for seniors over 70 who face tighter eligibility criteria. Brokers have access to specialty and regional markets that you’d never find shopping direct. The downside is that some brokers earn commissions that could create bias — ask upfront how they’re compensated.

My Final Take

The 2026 car insurance price shock for seniors is real, it’s significant, and it’s not going away on its own. But it is manageable — if you treat your insurance like the major expense it’s become and put in the 2–3 hours a year needed to shop it properly.

What I’d tell every driver over 65 right now: don’t accept your renewal passively. Don’t assume your current insurer is still your best option. Don’t skip the defensive driving course because it sounds like extra work. And don’t forget to ask about every discount you might be eligible for — because nobody’s going to volunteer that information unprompted.

The seniors I know who are beating this rate shock aren’t doing anything heroic. They’re just comparison shopping, stacking discounts, and treating their insurance review as the same kind of important annual task as a health checkup. That approach won’t eliminate the increases entirely — but it can cut them in half.

11 Responses

[…] 📌 For the full picture of the 2026 price shock affecting all seniors, read our main guide: 2026 Car Insurance Price Shock: What Every Driver Over 65 Needs to Know Now […]

[…] 📌 To understand how these increases affect drivers over 65 and beyond, check our detailed pillar article: 2026 Car Insurance Price Shock: What Every Driver Over 65 Needs to Know Now […]

[…] 📌 Learn more about the major rate increases seniors are facing this year in our pillar guide: 2026 Car Insurance Price Shock: What Every Driver Over 65 Needs to Know Now […]

[…] 📌 This topic is part of the bigger 2026 insurance crisis explained here: 2026 Car Insurance Price Shock: What Every Driver Over 65 Needs to Know Now […]

[…] 📌 For a complete overview of how the 2026 price shock is impacting senior drivers, see our main article: 2026 Car Insurance Price Shock: What Every Driver Over 65 Needs to Know Now […]

[…] 📌 Discover the full story behind these increases in our comprehensive guide: 2026 Car Insurance Price Shock: What Every Driver Over 65 Needs to Know Now […]

[…] 📌 These discounts are even more important during the current price shock. Read the full analysis here: 2026 Car Insurance Price Shock: What Every Driver Over 65 Needs to Know Now […]

[…] 📌 To understand why choosing the right company matters more than ever in 2026, read: 2026 Car Insurance Price Shock: What Every Driver Over 65 Needs to Know Now […]

[…] 📌 This comparison becomes even more critical when you see the full 2026 price shock explained here: 2026 Car Insurance Price Shock: What Every Driver Over 65 Needs to Know Now […]

[…] 📌 Learning these money-saving tips is essential during the 2026 price increases. See the big picture in our pillar article: 2026 Car Insurance Price Shock: What Every Driver Over 65 Needs to Know Now […]

[…] 📌 For deeper insight into why rates are rising and how to fight back, read our main guide: 2026 Car Insurance Price Shock: What Every Driver Over 65 Needs to Know Now […]