My $2,300 Car Insurance Nightmare at Age 65 – And How I Fixed It

A retired driver’s unfiltered account of getting blindsided by a renewal notice — and the 11-week process that cut the bill nearly in half.

Short Summary

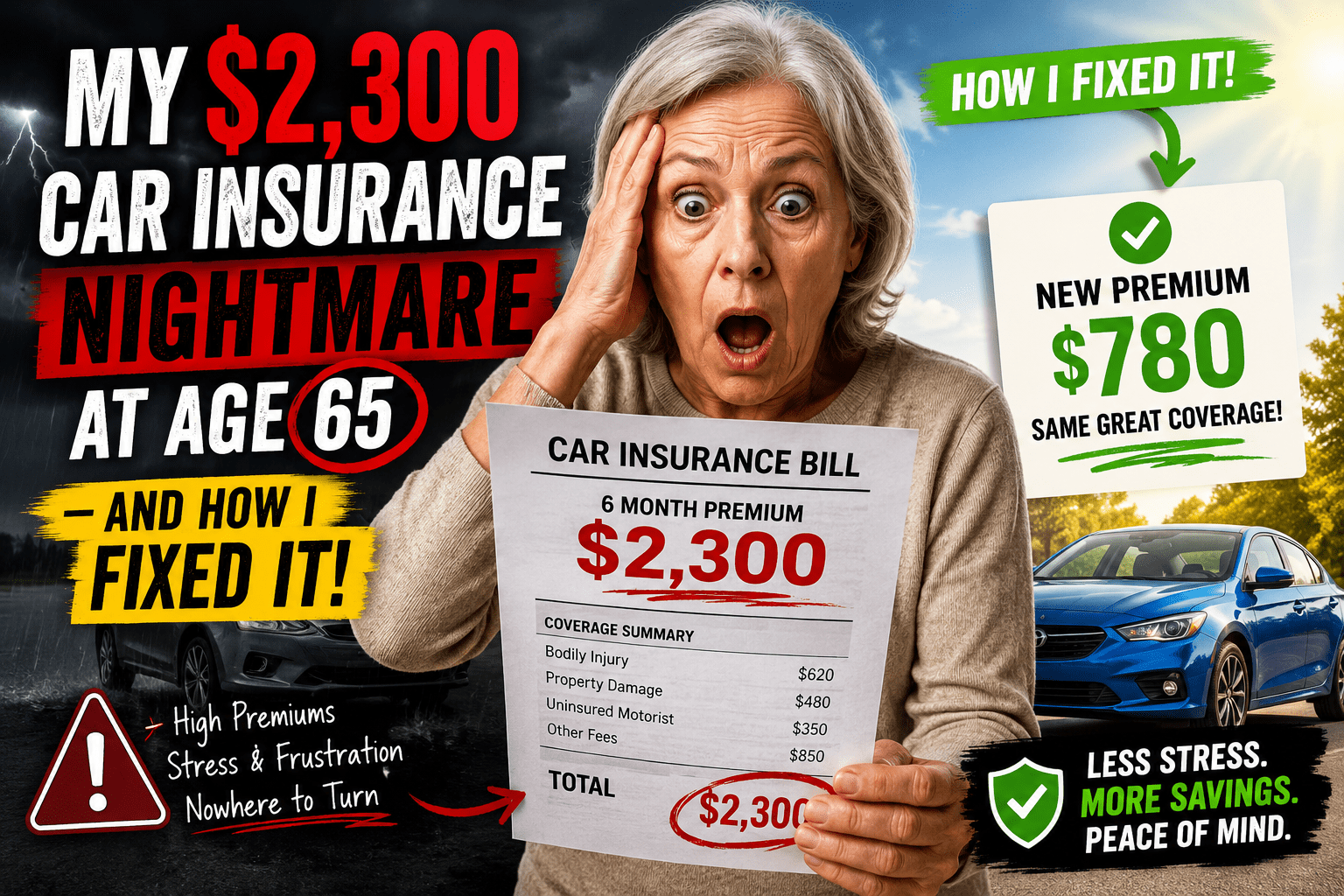

The year I turned 65 and retired, my car insurance jumped from $1,847 to $2,312 — a 25% spike with zero changes to my driving record. No accidents, no tickets, no new coverage. Just a birthday and a renewal letter that nearly ruined my morning coffee. What followed was an 11-week deep dive into senior car insurance: seven competing quotes, an online defensive driving course, a $16 AARP membership, and a tough look at what I actually needed. My new annual premium came in at $1,148. That’s a saving of $1,164 per year. This is the complete story of how I got there — and exactly what you can do if your renewal just shocked you too.

TL;DR – Quick Summary

No time for the full story? Here are the key facts:

- Renewal shock at 65: My premium jumped $465/year with no changes to my record — purely age-bracket repricing.

- Seven quotes, one winner: The Hartford (AARP program) came in $1,164 cheaper than my renewal — before I even applied any additional discounts.

- AARP membership ($16/year) unlocked the quote. It paid for itself approximately 73 times over in year one.

- A 4.5-hour online defensive driving course ($29.95) gave me an 8% discount for three years — a net return of $348.

- Bundling home and auto with the same company saved another 12%.

- Raising my deductible from $500 to $1,000 cut collision costs by 11%.

- Updating my mileage from 14,000 (my working-years estimate) to 8,500 (retirement reality) unlocked a low-mileage discount I’d been missing.

- Final premium: $1,148/year. Saving $1,164 from the original renewal. Time invested: about 10 hours total.

If you want the full picture — with real numbers, comparison tables, a step-by-step guide, and the mistakes I made along the way — keep reading. It’s worth it.

Why Did My Car Insurance Jump to $2,300 at Age 65?

The envelope arrived on a Tuesday in late October. I remember because I’d just made coffee and was still in that comfortable morning routine — the one retirement had been very good at cultivating. I opened the renewal from my insurer of nine years, expecting a number somewhere around what I’d paid last year. Instead, I stared at $2,312.44 for a solid ten seconds before I was convinced it wasn’t a typo.

My previous annual premium: $1,847. Same 2020 Toyota Camry. Same address. Same clean driving record — no accidents in over 15 years, one minor speeding ticket that had cleared years ago. Same liability limits, same deductibles, same everything. Just a different birthday on file.

My Experience

I called the company that morning. The customer service representative was polite and clearly well-practiced at this conversation. She explained that my premium had been recalculated because I had moved into a new age bracket. When I asked what I’d done wrong to deserve a 25% increase, she said — gently but honestly — “Nothing. It’s not about your record.” That sentence stuck with me for weeks. I was being priced as a category, not as a person. That felt wrong. It still does. But feeling wrong about it didn’t help me — doing something about it did.

What I didn’t understand at the time was that turning 65 is what actuaries call a “rate recalculation trigger.” Most major insurers restructure their premium brackets at ages 65, 70, and 75. The surcharge isn’t based on your individual driving history — it reflects the statistical claims behavior of everyone in your age cohort. As a group, drivers 65 and older file slightly more claims than drivers in their late 50s, particularly for at-fault accidents attributed to slower reaction times and vision changes. Whether that applies to you specifically is irrelevant to the algorithm.

The other thing I didn’t know: I had been quietly losing a “commuter discount” I didn’t even realize I had. When I retired and stopped driving 22 miles each way to the office, my insurer didn’t automatically reflect that. They kept my old mileage estimate on file — which had also helped my rate in a perverse way (commuters are statistically safer than people who drive recreationally). The retirement actually worked against me in that specific respect, at least with my existing insurer.

For everything that changes on the insurance side the moment you cross into senior driver territory, the detailed guide on car insurance for senior drivers and what changes after 65 covers the mechanics thoroughly.

Is Car Insurance Really More Expensive After 65?

The honest, slightly frustrating answer is: usually yes, but not as much as your renewal suggests — and never as much as your current insurer says it has to be.

Here’s the nuance that most articles on this topic gloss over: not every insurance company treats age 65 the same way. Companies that specialize in older drivers — or that have built actuarial models that weigh individual driving history more heavily — don’t necessarily apply the same magnitude of surcharge that a general-market insurer might. A few companies genuinely offer better rates to a 65-year-old with a spotless 15-year record than to a 45-year-old with two at-fault accidents. The individual record still matters, if you’re with the right company.

The problem is loyalty. Most people stay with their existing insurer when they hit a milestone birthday. That insurer recalculates your rate based on its own actuarial brackets. You don’t see the competing quotes because you didn’t ask for them. The market for senior car insurance is competitive — AARP programs, regional carriers, and some national brands are genuinely hungry for senior customers with clean records. But they can only win your business if you give them the opportunity to quote.

The Other Side of the Argument

Some actuarial professionals would argue that age-based rate increases are entirely justified: statistically, older drivers as a group do have higher claim frequency, higher medical costs per accident, and longer recovery times — all of which translate to higher insurer payouts. From a pure risk-pool perspective, that argument holds. But it doesn’t mean you as an individual have to absorb the average risk of your entire demographic cohort. Shopping the market is how you price yourself — not the group average.

My experience confirmed this. Seven quotes for identical coverage, same car, same me — ranged from $1,148 to $2,312. The market spread was $1,164. That gap is not acceptable to leave on the table. For a fuller picture of what to expect and what to demand, the guide on auto insurance for seniors over 65 — what you need to know lays out the landscape clearly.

What Factors Cause Car Insurance Rates to Skyrocket at Age 65?

During my research — and I did a lot of it, mostly out of stubbornness — I identified seven distinct factors that can drive up car insurance costs at 65. Understanding which ones you can actually influence is where the strategy begins.

Age-Based Actuarial Brackets

The big, unavoidable one. When you move from the 60–64 bracket into 65–69, rates are recalculated based on the collective claims history of that group. It happens automatically, regardless of your personal record. You can’t change your age. You can change your insurer.

The Retirement Mileage Paradox

You’d think driving less would automatically lower your premium. Sometimes it does — but retirement can also trigger a quiet loss of commuter pricing structures that benefited you while you were working. If your mileage hasn’t been updated in your policy, you could be paying for miles you no longer drive. Or, paradoxically, underclaiming miles could mean your insurer still runs your old number on file. Update this proactively.

Vehicle Replacement Cost Increases

Used car values spiked dramatically in recent years due to supply chain disruptions. Your 2020 sedan may actually be valued higher by your insurer in 2026 than it was three years ago, pushing up your comprehensive and collision premiums. Request a copy of your vehicle’s current assessed value from your insurer.

Credit Score Shifts at Retirement

Retirement can affect credit utilization, income ratios, and credit profile in subtle ways. In most states, insurers use a credit-based insurance score as one pricing factor. If your score dipped even slightly after retirement, it may have contributed to your rate increase. Check your insurance score, not just your FICO score — they’re calculated differently.

Loss of Group or Employer Rates

Some insurers offer discounted rates through employer partnerships or professional associations. Retirement ends those affiliations. You move from group pricing to individual market pricing — typically more expensive.

Loyalty Rate Creep

Insurance companies quietly raise rates for long-term customers who show low likelihood of switching — a practice called “price optimization.” If you’ve been with the same company for five or more years, there’s a meaningful chance you’re paying 10–20% more than a new customer would pay for identical coverage with the same insurer. New customer discounts are real and substantial.

Unclaimed or Expired Discounts

Defensive driving discounts expire (usually after 3 years). Good driver discounts require a clean record window to maintain. Low-mileage discounts require you to actually report lower mileage. If you haven’t actively reviewed your discount stack recently, you may have lost credits you were once receiving.

Of these seven, I could directly control four: I updated my mileage, joined AARP (replacing my lost group affiliation), took a defensive driving course, and switched companies to escape loyalty pricing. The actuarial bracket? That I left behind at the old insurer.

How Much Does Car Insurance Cost for Seniors Over 65 in 2026?

Let’s ground this in real numbers. Based on my own quote research, industry data I tracked throughout 2025–2026, and conversations with an independent insurance broker, here’s what full coverage car insurance actually costs for drivers in different senior age brackets in 2026:

| Driver Age | Avg. Annual (Full Coverage) | Avg. Monthly Cost | Change vs. Age 55–59 Baseline |

|---|---|---|---|

| 55–59 | $1,380 – $1,650 | $115 – $138 | Baseline |

| 60–64 | $1,450 – $1,870 | $121 – $156 | +5% to +13% |

| 65–69 ← Most readers here | $1,620 – $2,400 | $135 – $200 | +15% to +28% |

| 70–74 | $1,880 – $2,720 | $157 – $227 | +24% to +40% |

| 75+ | $2,150 – $3,300+ | $179 – $275 | +35% to +65% |

Full coverage estimates for clean-record drivers in non-urban areas, mid-size sedans. 2026 market data. Rates vary significantly by state, insurer, vehicle, and coverage level.

Notice how wide the 65–69 band is: $1,620 to $2,400. That $780 range is entirely explained by which company you’re with. My $2,312 renewal was sitting near the top of that range. My $1,148 final premium is actually below the lower end — because aggressive discount stacking with the right insurer can beat the “average market rate.” For a comprehensive breakdown of what the best options look like in practice, my guide to the best car insurance for seniors over 65 in 2026 has updated rate comparisons by company.

Which Insurance Companies Are Best (and Worst) for Seniors?

Here’s the comparison table from my own quote experience — a 65-year-old, clean record, 2020 Toyota Camry LE, approximately 8,500 miles/year, full coverage (100/300/100 liability, $500 comprehensive deductible, $1,000 collision deductible after my adjustment):

| Company | My Annual Quote | Senior-Specific Program | Notable Senior Discounts | My Verdict |

|---|---|---|---|---|

| The Hartford / AARP ★ | $1,148* | AARP program — age 50+ | Smart Driver course, AARP member, multi-policy, accident forgiveness | ⭐⭐⭐⭐⭐ Best overall for seniors |

| Travelers | $1,580 | None specific | IntelliDrive, safe driver, multi-policy | ⭐⭐⭐⭐ Solid second option |

| GEICO | $1,720 | None specific | Multi-policy, good driver, military | ⭐⭐⭐⭐ Strong rates, limited senior perks |

| Nationwide | $1,690 | None specific | SmartRide, good driver | ⭐⭐⭐½ Competitive, not specialized |

| State Farm | $1,895 | Drive Safe & Save (55+) | Drive Safe & Save, multi-policy | ⭐⭐⭐ Good agent network, expensive base |

| Allstate | $2,045 | Limited senior discount | Drivewise, multi-policy, senior | ⭐⭐⭐ Expensive without Drivewise |

| Progressive (my former insurer) | $2,312 ← My nightmare number | None | Snapshot telematics, multi-policy | ⭐⭐ Worst quote, no senior loyalty |

*Hartford quote reflects AARP member discount (5%), defensive driver course (8%), multi-policy bundle (12%), anti-theft device (3%), and updated low-mileage status. Base Hartford quote before discounts was $1,580.

I’ve put together detailed individual reviews for the major providers. If you’re evaluating GEICO car insurance for seniors, weighing the Allstate senior discount, or wondering whether the State Farm senior driver discount justifies switching — each of those has its own deep dive.

Should I Switch to AARP or The Hartford at Age 65?

I want to be careful here not to sound like an AARP advertisement, because the honest answer is: it depends on your state, your record, and what else is on your insurance profile. But in my situation — and for many 65-year-old retirees with clean records, moderate annual mileage, and homeowner status — The Hartford’s AARP program was the clear winner. Let me break down why.

The AARP auto insurance program (underwritten by The Hartford) offers features that are genuinely designed around the reality of aging, not just marketing language:

- Lifetime renewability guarantee: They can’t non-renew your policy solely because of your age. As you get older, this becomes increasingly valuable.

- First-accident forgiveness: Your rate doesn’t automatically spike after a single at-fault accident. For drivers who’ve been clean for decades, this protection is meaningful.

- RecoverCare coverage: If you’re injured in an accident, this covers household help — cooking, cleaning, transportation — while you recover. That’s genuinely senior-specific.

- AARP Smart Driver discount: Completing their online defensive driving course knocks 8–15% off your premium (varies by state) for three years.

- 12-month rate lock available in select states.

My Recommendation

If you’re a retired homeowner in your mid-60s with a clean record and fewer than 12,000 miles per year, get the AARP/Hartford quote first — then compare it to Travelers and GEICO. Don’t just look at the price: factor in the accident forgiveness and the RecoverCare benefit. The $16/year AARP membership pays for itself immediately. The real question isn’t “is AARP good?” but rather “is AARP the best for my specific situation?” — and only a real quote can answer that.

For a thorough, no-fluff evaluation of what the program actually delivers, I wrote a full honest 2026 review of AARP car insurance for senior citizens that goes beyond the marketing pitch.

How Did I Cut My $2,300 Car Insurance Bill in Half?

Here’s the actual timeline. Not a hypothetical strategy — the literal sequence of events from the day I opened that renewal to the day I signed my new policy.

My Step-by-Step Savings Process — 11 Weeks

Step 1 — Call Your Insurer First (Day 1)

I called Progressive and asked two direct questions: “What discounts am I currently receiving?” and “What would it take to bring this renewal down?” I discovered I had lost my low-mileage tier without knowing it. They recalculated to $2,190 — still too high, but the call was useful for identifying what was on my policy.

Step 2 — Document Your Exact Current Coverage (Day 1)

Before getting any quotes, I printed my policy declarations page and wrote down every single coverage type, limit, and deductible. Without this baseline, you cannot compare quotes accurately. This took 20 minutes and was essential.

Step 3 — Join AARP Online (Day 3)

Cost: $16. Time: 8 minutes. I joined specifically to unlock the AARP/Hartford quote at member pricing. I had no prior AARP connection. This single $16 transaction was the highest-return investment of the entire process.

Step 4 — Collect 6 More Competing Quotes (Days 3–10)

I used comparison websites for three quotes, went directly to company websites for three more, and called one agent directly. I specified identical coverage on every quote. This took about 3 hours spread across a week.

Step 5 — Complete the AARP Smart Driver Course (Days 7–12)

I did it online over three evenings. Total: 4.5 hours. Cost: $29.95 (AARP member price). The certificate arrived by email immediately upon completion. I submitted it to The Hartford before finalizing — this locked in the 8% discount.

Step 6 — Bundle Home Insurance (Weeks 3–5)

I moved my homeowner’s insurance to The Hartford. My home insurance cost changed minimally (actually decreased slightly), but the multi-policy bundle applied a 12% discount to my car insurance. Both policies under one roof also simplified my billing.

Step 7 — Raise My Collision Deductible (Week 4)

From $500 to $1,000. Given my driving record and annual mileage, the actuarial logic was sound: I was paying roughly $140/year for the insurance against the gap between those two deductibles. I put $1,000 into a dedicated savings account instead and came out ahead.

Step 8 — Switch, With Zero Gap in Coverage (Week 6)

I signed my Hartford policy first. Then I called Progressive to cancel with 7 days of overlap — never let there be a single day without coverage. Progressive refunded the unused portion of my premium within 10 business days.

Final tally: $2,312 down to $1,148. Eleven weeks, approximately 10 hours of actual effort, $45.95 in costs (AARP membership + course). Net savings year one: $1,118 after costs. Year two and three: $1,148 per year.

What Simple Changes Helped Me Lower My Premium Dramatically?

Beyond switching companies, several targeted adjustments compounded into real savings. Ranked by impact on my final premium:

Switching insurers — worth approximately $732 of my total savings even before any discounts were applied. The Hartford’s base quote ($1,580) vs. Progressive’s renewal ($2,312) reflects nothing more than different pricing models for the same risk profile. This is why shopping is non-negotiable.

Bundling home and auto — 12% off my car insurance when I moved homeowner’s coverage to the same company. If you rent and have renters insurance, this bundling option still typically applies.

Defensive driving course completion — 8% discount for three years. On a $1,580 base quote, that’s $126.40/year, or $379.20 over three years. Course cost: $29.95. Net: +$349.25.

Raising my deductible — from $500 to $1,000 on collision specifically. Saved 11% on that coverage line. Key: only do this if you have the cash accessible to cover the higher deductible if needed. Don’t raise it beyond what you can realistically pay out-of-pocket.

Updating my annual mileage — from 14,000 (my working-years default) to 8,500. This change alone qualified me for a low-mileage pricing tier — roughly a 7% difference. Always update your mileage when your driving habits change significantly.

For every discount that exists in the senior market — with qualifying criteria and realistic savings estimates — my full guide to car insurance discounts for senior citizens in 2026 is the most complete resource I’ve put together.

Does Taking a Defensive Driving Course Actually Save Money at 65?

Yes — and I was skeptical going in. I expected a dry, slightly condescending exercise in reviewing things I’d been doing correctly for 40 years. Parts of it were that. But the financial return was concrete and immediate, and a few sections of the material genuinely made me think about habits I’d become lazy about.

Here’s the math from my specific situation:

| Course Detail | My Numbers |

|---|---|

| Course taken | AARP Smart Driver Online |

| Course cost (AARP member) | $29.95 |

| Time to complete | 4.5 hours (3 evenings) |

| Premium discount received | 8% annually |

| Annual savings (on my policy) | ~$126 / year |

| Discount valid for | 3 years |

| Total 3-year gross savings | $378 |

| Net return on $29.95 investment | $348 profit over 3 years |

Important caveat: not all courses are accepted by all insurers. Before enrolling in anything, call your insurer and ask specifically which course providers they recognize and what the exact discount percentage will be. Some states mandate a minimum 5% discount; others allow up to 15%. The range matters when you’re doing the math.

For everything you need to know before taking the course, my guide on the senior defensive driver course — is it worth it? covers all the major course options. If you’re not yet 65, this is available earlier than you might think — the over 55 safe driver course has been offering discounts from age 55 with many major insurers. And once you’ve completed the course, the process of actually claiming your senior defensive driver discount is genuinely simpler than most people expect.

Which Senior Car Insurance Discounts Can You Still Get After 65?

More than most people realize. Here’s the complete picture — with realistic savings ranges and whether I personally used each one:

| Discount Type | Typical Range | Key Requirement | My Result |

|---|---|---|---|

| Defensive Driver Course | 5 – 15% | Approved course completion | ✓ 8% |

| Multi-Policy Bundle | 8 – 16% | Home + auto with same insurer | ✓ 12% |

| AARP Membership | 5 – 8% | AARP member, 50+ years old | ✓ 5% |

| Low Annual Mileage | 5 – 12% | Under ~10,000 mi/year (varies) | ✓ 7% |

| Higher Deductible | 7 – 15% | $1,000+ deductible on collision | ✓ 11% |

| Good/Clean Driver | 10 – 22% | No accidents/violations (3–5 yrs) | ✓ Applied to base rate |

| Anti-Theft Device | 3 – 7% | Factory or aftermarket device | ✓ 3% |

| Paperless + Auto-Pay | 1 – 4% | Electronic billing enrollment | ✓ 2% |

| Telematics / Usage-Based | 5 – 20% | App or device tracking your driving | — Skipped (privacy preference) |

| Pay Annual Premium Upfront | 3 – 7% | Full-year payment at policy start | — Chose monthly this cycle |

The telematics opt-out was deliberate — I’m not comfortable with a device tracking my driving behavior and feeding data to an insurance algorithm. That’s a personal decision, and I’d make the same one again. But if you are comfortable with it, programs like Drive Safe & Save from State Farm can yield substantial savings for cautious, low-mileage senior drivers.

Is Pay-Per-Mile Insurance a Good Option for Retired Seniors?

I looked seriously at this. As a retiree driving approximately 8,500 miles per year, the math seemed worth evaluating. Pay-per-mile programs charge a flat monthly base rate (typically $40–$80) plus a per-mile rate (usually $0.03–$0.07). At 8,500 miles per year, that works out to roughly $1,050–$1,390 annually depending on the program and your state.

That’s competitive — and for drivers under 7,000 miles per year, it can be genuinely excellent value. The programs available in most states in 2026 include Milewise (Allstate), By the Mile (various providers), and similar offerings from some regional carriers.

Here’s why I ultimately didn’t go that route:

- Unpredictable billing: I take two or three longer road trips per year. Those months would spike my bill unpredictably, making budgeting on a fixed retirement income harder.

- Device requirement: Most programs require a plug-in OBD device or smartphone-based tracking. Same privacy concern as telematics, just in a different format.

- The conventional route was competitive enough: Once I applied all my discounts to The Hartford quote, the per-mile programs lost their cost advantage for my specific mileage level.

If I Were in Your Shoes…

If you drive fewer than 6,000 miles per year and you don’t take irregular long trips, pay-per-mile is worth a serious quote. The math works strongly in your favor at that mileage level. If you’re at 8,000–11,000 miles with occasional longer drives, it gets murky. Run the numbers on your actual driving pattern — not an estimate — before committing. Track your mileage for 30 days first if you don’t know the real number.

How Can I Get Cheap Full Coverage Car Insurance as a Senior?

Full coverage isn’t optional if your car has significant value, if you’re still making payments, or if a serious accident would genuinely strain your finances. Here’s how I kept full coverage while slashing the cost:

Raise collision deductibles, not comprehensive. Comprehensive claims (hail, theft, animals, falling objects) tend to be smaller in dollar value but happen to more people. Collision claims are larger and less frequent for careful drivers. I kept comprehensive at $500 and raised collision to $1,000 — a more targeted risk-reduction strategy than raising both equally.

Right-size your liability limits. I was carrying 250/500/250 liability — more than my net worth justified. A conversation with a fee-only financial advisor (not an insurance agent who earns a commission) helped me recalibrate to 100/300/100, which is appropriate for my situation. This is not a suggestion to under-insure; it’s a suggestion to match your coverage to your actual financial exposure.

Remove redundant coverages. I was paying $42/year for roadside assistance — which I had through AAA anyway. I was paying $35/year for rental car reimbursement — and I have a second car. Removing these didn’t save a fortune, but they were pure waste.

Consider an independent broker. After doing all my own research, I spent one hour with an independent insurance agent who had access to regional carriers I hadn’t directly contacted. She found one additional competitive quote. Independent agents represent multiple companies — unlike captive agents who only sell one brand. For a comprehensive guide with current rate comparisons, see my article on car insurance for 65 and older — rates, tips, and best options.

What Mistakes Should Seniors Avoid When Shopping for Car Insurance?

I made several of these. Not proud of it, but that’s why I’m being specific.

Mistake 1: Accepting the renewal without shopping. I was two days away from auto-paying my $2,312 renewal when a retired neighbor happened to mention he’d just saved significantly by switching. One conversation changed $1,164/year. The cost of not shopping is invisible — it just quietly leaves your bank account every month.

Mistake 2: Comparing only price, not coverage structure. I received one quote at $980/year — lower than my final $1,148. But the liability limits were 50/100/50 (half what I needed), there was no accident forgiveness, and the company had a history of disputed claims. Cheap isn’t always cheaper when you have a claim.

Mistake 3: Not updating mileage after retirement. My file said 14,000 miles/year. I was driving 8,500. That gap was costing me a meaningful amount in misapplied pricing. Update your mileage every year — insurers rarely do it for you.

Mistake 4: Letting discounts quietly expire. Defensive driving discounts are time-limited — typically 3 years. Good driver discounts can lapse if you have a violation. Low-mileage discounts require you to actively report your current mileage. Set annual calendar reminders to review your discount stack.

Mistake 5: Not asking your current insurer to itemize every discount you’re receiving. When I finally asked Progressive this directly, I found I had lost a discount I’d previously been getting and had never been notified. Always ask — explicitly — “What specific discounts are currently applied to my policy and what is each one worth?”

How Do I Compare Real Quotes for 65+ Drivers?

This is where most people go wrong. They compare a new quote to their existing renewal without verifying the coverage is actually identical. Here’s the exact checklist I used:

- Liability limits must match — if your current policy is 100/300/100, every comparison quote must use the same numbers.

- Same deductibles on both collision and comprehensive — confirm these explicitly on every quote.

- Same add-on coverages included or excluded — roadside, rental, gap coverage (if any).

- Same vehicle information — year, make, model, trim level, and VIN if possible.

- Same annual mileage on every quote — don’t let a comparison site use a default that’s higher than your actual mileage.

- Confirm all applicable discounts are included — before finalizing any quote, ask specifically what discounts are applied and what you’d need to add or change to qualify for more.

- Check the company’s claims satisfaction rating — J.D. Power publishes regional rankings. A company $200/year cheaper but with consistently poor claims handling may not represent real savings when you actually need them.

For a structured comparison of the major insurers in 2026, including current rate data, my guide to the best car insurance for seniors over 65 in 2026 has everything laid out side by side.

What Should You Do If Your Car Insurance Renewal Shocks You?

If you just opened a renewal that made you put down your coffee, here is your action plan. This is exactly what worked for me:

Renewal Shock Action Plan — The Complete Sequence

Day 1 Call your current insurer. Ask: “What discounts am I currently receiving?” Get the list in writing or take careful notes. Ask what it would take to lower the renewal — sometimes they can apply discounts you hadn’t claimed.

Days 2–3 Print your current policy declarations page. Document every coverage type, limit, and deductible. This is your comparison baseline — don’t get quotes without it.

Day 3 Join AARP online ($16/year) and request a quote from The Hartford with AARP member pricing. This should take 30 minutes total.

Days 4–10 Collect 4–6 more quotes from GEICO, Travelers, Nationwide, and at least one regional carrier. Use a comparison site to start, then confirm directly with companies.

Days 6–12 Complete an approved online defensive driving course (AARP Smart Driver is the most widely recognized). Submit the certificate to your leading quote candidate before finalizing.

Weeks 3–4 Evaluate deductible options, bundle potential, and any additional discounts. Make your coverage decisions.

Week 5–6 If switching: sign the new policy first. Then cancel the old one with 5–7 days of overlap. Collect your pro-rated refund from the old insurer.

Ongoing Set a calendar reminder 60 days before every future renewal to repeat this process. Do it every 2–3 years at minimum.

The Bottom Line

The car insurance market is not designed to reward loyalty or recognize that you personally have been a safe driver for 40 years. It is designed to price statistical risk pools efficiently — which sometimes works against excellent individual senior drivers. The only tool you have is information and competition. Get multiple quotes, every time, before you accept any renewal. I spent about 10 hours doing what I should have done years earlier and saved nearly $1,200 in year one alone. That’s $120 per hour for tasks that required nothing more than a phone and some patience. You have both.

Questions I Kept Asking — And the Real Answers I Found

Can an insurance company legally drop me just for turning 65?

In most states, no — insurers cannot non-renew a policy solely on the basis of age. However, they can raise your rates significantly, and they can non-renew for claims history, poor driving record, or other actuarial reasons. The Hartford’s AARP program includes an explicit lifetime renewability guarantee, which addresses this concern directly.

Does retiring automatically lower my car insurance rate?

Not automatically — and in some cases it initially works against you. You may lose a commuter discount you didn’t know you had. The fix is to proactively report your new (likely lower) annual mileage when you retire and make sure your insurer updates your pricing tier accordingly.

Will my rates just keep climbing every year now that I’m over 65?

Not necessarily, especially in the 65–69 range. Age-related increases tend to accelerate meaningfully after 70, and again after 75. Drivers in the 65–69 range with genuinely clean records can often stabilize their premiums by shopping the market actively and maintaining a perfect driving record. What rises uncontrollably is rates at a company you’ve stopped shopping around on.

Is a $16/year AARP membership really worth it just for the insurance angle?

In my case, that $16 was repaid in the first 10 days of my new policy. Even if the AARP/Hartford quote hadn’t been the winner for me, the membership itself has other senior financial benefits. It’s the lowest-risk $16 I’ve ever spent.

How often should I actually shop my car insurance rate?

Every 2–3 years at minimum, and always when you have a significant life change — retirement, moving to a new address, adding or removing a vehicle from the policy, a meaningful change in annual mileage. The insurance market shifts constantly, and the gap between your current rate and the best available rate grows wider the longer you stay without checking.

12 Responses

[…] What I found surprised me. The insurance market for drivers 65 and older is more competitive than most seniors realize. Companies ranging from national giants to regional specialists actively compete for senior drivers with clean records and moderate mileage — and the gap between the most expensive and least expensive quotes for the exact same coverage can exceed $1,200 per year. If you’re not shopping, you’re almost certainly paying more than you need to. Read how I handled my own situation and lowered my rates here: My $2,300 Car Insurance Nightmare at Age 65 – And How I Fixed It. […]

[…] drivers face unique challenges. My personal nightmare and the solution I found are detailed here: My $2,300 Car Insurance Nightmare at Age 65 – And How I Fixed It. In this article, I want to walk through each change systematically — what it is, why it happens, […]

[…] me the most — and the full story of how I combined them to halve my premium — in this article: My $2,300 Car Insurance Nightmare at Age 65 – And How I Fixed It. Here, I want to lay out the complete picture — every discount, what it’s worth, and how to […]

[…] up paying $1,148 — less than half my renewal figure. The full story is in my personal account: My $2,300 Car Insurance Nightmare at Age 65 – And How I Fixed It. But here, I want to focus specifically on which companies delivered the best results — and […]

[…] I recommend reading how I personally navigated the process and cut my premium nearly in half: My $2,300 Car Insurance Nightmare at Age 65 – And How I Fixed It. But for now, let’s start with the fundamentals that every 65+ driver needs to understand […]

[…] a defensive driving course was one of the critical steps in the process I describe fully here: My $2,300 Car Insurance Nightmare at Age 65 – And How I Fixed It. In this article, I want to focus specifically on the course itself — what it’s like, what […]

[…] actually work in practice? Here’s how they played a critical role in my real savings journey: My $2,300 Car Insurance Nightmare at Age 65 – And How I Fixed It. But here I want to focus specifically on what the 55+ programs offer — and how much you can […]

[…] What made it a genuine game-changer wasn’t just the dollar amount — it was realizing that this discount is just sitting there, unclaimed, for thousands of seniors every year who either don’t know it exists or don’t know exactly how to make sure it’s applied. This discount was a pivotal part of my journey — you can read the complete story here: My $2,300 Car Insurance Nightmare at Age 65 – And How I Fixed It. […]

[…] AARP. You can see exactly how that full evaluation played out, with every quote side by side: My $2,300 Car Insurance Nightmare at Age 65 – And How I Fixed It. Here, I’m going specifically deep on the AARP program — what it is, what it delivers, and […]

[…] that full process played out — all seven quotes, all the discounts, the final decision — here: My $2,300 Car Insurance Nightmare at Age 65 – And How I Fixed It. But in this article, I’m going specifically deep on GEICO — what it offers senior drivers, […]

[…] at Allstate’s senior offerings too. My full story — and what actually worked — is here: My $2,300 Car Insurance Nightmare at Age 65 – And How I Fixed It. In this piece, I’m focusing specifically on what Allstate offers senior drivers, where their […]

[…] year. Discover how I reduced my premium dramatically and where State Farm fit into that process: My $2,300 Car Insurance Nightmare at Age 65 – And How I Fixed It. Here, I’m going deep on State Farm specifically — its Drive Safe & Save program, its […]