Best Car Insurance in Florida for Seniors – Honest Comparison

Most comparison sites rank insurers by whoever pays the highest affiliate commission. This one doesn’t. Here’s what a genuine head-to-head comparison of Florida’s top senior auto insurers actually looks like.

Short Summary

This is a direct, honest comparison of the top car insurance carriers for Florida seniors — evaluated on rates, discount structure, claims handling, customer experience, and total value. Not on which company pays us the most to be featured first. You’ll find a comprehensive head-to-head table, scenario-based comparisons for real driver profiles, and my personal verdict on where most Florida seniors should actually be looking in 2026. Spoiler: the answer is almost never the carrier you’ve been with for the past decade without questioning it.

Why Most Car Insurance Comparisons for Florida Seniors Miss the Point

I want to tell you what happened with my uncle Raymond before I get into any of the numbers.

Raymond is 77. He lives in Ocala, drives a 2020 Toyota Camry, and has been on a fixed income for years. A few months ago, he called me genuinely confused. He had gone to one of those big comparison websites — the ones with the TV commercials and the friendly logos — and run his information. The “recommended” carrier at the top of his results was charging $3,480 per year. The next three on the list were between $3,100 and $3,400. He thought this was just the market rate for a man his age in Florida.

I told him to give me an hour. I ran direct quotes from four carriers, applied Raymond’s mature driver course certificate (he had completed AARP Smart Driver two months earlier and never submitted it anywhere), updated his mileage to reflect his actual retirement driving of about 5,200 miles per year, and bundled with his homeowners policy.

State Farm came back at $2,030 per year. GEICO at $2,115. The carrier at the top of that comparison site’s list was charging Raymond 71% more than State Farm for identical coverage.

Why? Because those comparison sites rank by commission, not by value. This comparison does not do that. Here’s what the real picture looks like.

For the complete strategy guide on how Florida seniors can save thousands by stacking discounts and shopping strategically, see: The Car Insurance Secret Florida Seniors Are Using to Save Thousands.

What This Comparison Covers — and What It Doesn’t

Before I get into the data, let me be clear about scope. This comparison evaluates:

- Estimated annual premiums for Florida seniors across representative profiles (clean record, 55–74 years old, typical FL ZIP codes)

- Availability and generosity of senior-specific discounts (mature driver course, low-mileage, bundling)

- Claims handling reputation based on J.D. Power satisfaction scores and Florida OIR complaint data

- Accessibility and service quality (local agents, phone service, digital tools)

- Rate stability over time (how much do rates typically change after a clean renewal?)

What this comparison does not do: quote your specific rate. Your rate depends on your ZIP code, credit-based insurance score, exact age, vehicle, coverage levels, and claims history. The figures here are representative, not personal quotes. Always get direct quotes from each carrier for your specific situation.

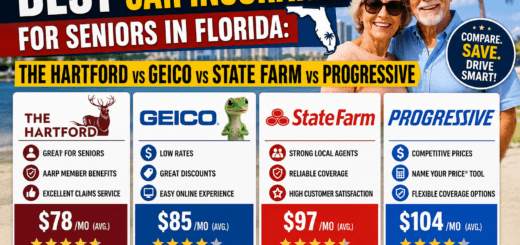

Head-to-Head Comparison: Best Car Insurance in Florida for Seniors

Representative profile: 68-year-old Florida senior, clean 5-year record, full coverage, 2019–2021 sedan, ~7,500 miles annually. Coverage: 100/300/100 liability, $500 deductibles, comprehensive + collision included.

*J.D. Power Auto Insurance Study scores are illustrative based on general industry performance tiers. Actual scores vary by region and study year. Rate estimates based on representative senior profile; your rates will vary. USAA scores above are consistently highest nationally but eligibility is restricted to military community.

Real Scenario: The Same Senior, Three Different Quotes

Abstract tables only go so far. Let me walk through a realistic scenario to show how the same Florida senior can get dramatically different quotes depending on where they look and what discounts are applied.

The Scenario: Meet Dorothy, Age 72, Boca Raton

- 👤 Age: 72 | Retired nurse

- 🚗 Vehicle: 2021 Toyota Camry (full coverage)

- 📍 Location: Boca Raton, FL (higher-cost South Florida market)

- 📌 Annual mileage: 6,200 miles

- ✅ Driving record: Clean for 7+ years

- 🎓 AARP Smart Driver course: Completed 3 months ago, certificate not yet submitted

- 🏠 Homeowner: Yes

The difference between Scenario 1 and Scenario 3: $1,560 per year. Same coverage. Same driver. Different choices.

Dorothy’s situation is not unusual. I see this pattern repeatedly — seniors sitting on completed certificates they’ve never submitted, accurate low-mileage data they’ve never reported, and bundling opportunities they’ve never explored. The savings are there. They just require action.

My Honest Verdict on Each Carrier

Beyond the numbers, here’s my unfiltered take on each major carrier based on real observations:

USAA: As good as advertised — for those who qualify

I have never helped an eligible USAA member find a meaningfully better deal elsewhere. If you qualify, the conversation starts and ends here. Their rates, claims process, and customer service all hold up under scrutiny. My only frustration: too many veterans don’t realize their family members also qualify, or don’t know they qualify themselves. Check before assuming you don’t.

State Farm: The best balance of price and service for most Florida seniors

If USAA is off the table, State Farm is my default recommendation for the majority of Florida seniors. Competitive rates, excellent agent network, and a claims experience that I have personally seen handled well multiple times. The post-incident rate increase is the main watch-out — but for seniors with clean records, that risk is low.

GEICO: Great value if you’re comfortable going digital

For seniors who want the best rate and are comfortable managing everything by phone or app, GEICO is often the right call. The discount stacking potential is impressive. The absence of a local agent relationship is a real drawback for people who prefer in-person support, but for uncomplicated situations it rarely matters.

Travelers: Genuinely competitive for Florida homeowners who bundle

Travelers is where the bundling math most often works in the policyholder’s favor. If you own a Florida home and are willing to evaluate home + auto together, Travelers should be in your final comparison. On auto alone without bundling, they’re less compelling.

Progressive: Worth it specifically for low-mileage retirees willing to use Snapshot

Snapshot is a genuinely good deal for the right senior — someone who drives under 8,000 miles per year, primarily during daytime hours, and with smooth braking habits. For that profile, Progressive’s total cost can be competitive with State Farm. The program works less well for anyone with occasional highway driving where hard braking might occur.

Allstate: Higher base rates undermine the discount programs

Allstate’s discount programs are real and reasonably well-structured. The problem is that their base rates for seniors in most Florida markets run noticeably higher than State Farm or GEICO. Even after applying Drivewise and the mature driver discount, the final number is often still above what competitors offer without those programs. Allstate makes sense when their home + auto bundle specifically competes in your region — which happens occasionally but not reliably.

Liberty Mutual: Rarely the right answer for Florida seniors

I include Liberty Mutual for completeness, but I rarely find them competitive for Florida seniors without significant bundling. Their RightTrack telematics program is solid for low-mileage drivers, but their base rates and overall structure are not optimized for the Florida senior market. Worth a quote for your specific situation, but not my starting recommendation.

Questions Worth Asking Before You Compare

Should I use a comparison website or go directly to carriers?

Both have value, but with an important caveat about comparison sites: their results are influenced by which carriers pay commissions to be featured. For the most accurate picture, always get at least two or three direct quotes from carriers you’ve identified as competitive — rather than relying solely on comparison site rankings. Use comparison sites to generate an initial list, then go direct for your final comparison.

How much should coverage limits affect my comparison?

Significantly. Make sure you’re comparing the same coverage levels across all carriers. A carrier that looks cheaper may be quoting lower liability limits, a higher deductible, or less robust uninsured motorist coverage. Ask each carrier to quote on the exact same coverage structure so you’re comparing apples to apples. I recommend at least 100/300/100 liability and $500 deductibles for most Florida seniors.

Is it worth switching if the savings are only $200–$300 per year?

This depends on your situation. If the savings are $200–$300 at a carrier with similar or better service quality, I’d generally say yes — over five years that’s $1,000–$1,500. If the savings are marginal ($100 or less) and your current carrier has an excellent claims track record you’ve personally experienced, the stability of an established relationship may be worth more. The rule I use: anything above $400/year in confirmed savings is nearly always worth switching for.

Conclusion

Raymond is now with State Farm. He pays $2,030 per year, down from the $3,480 that “comparison site” was pointing him toward. He has the same coverage, a local agent he can call, and the knowledge that his mature driver certificate is properly applied to his account. The comparison didn’t require special knowledge or expensive advice — it just required looking honestly at the right carriers with all the relevant discounts in the picture.

That’s what this comparison is designed to help you do. The best car insurance in Florida for seniors is rarely where the loudest advertising is. It’s where the math actually works in your favor — with your real numbers, your actual discounts, and your specific situation.

See the Full Savings Strategy

This comparison gives you the carrier landscape. Our main guide shows you exactly how to stack every discount and maximize your savings:

→ The Car Insurance Secret Florida Seniors Are Using to Save Thousands