Cheapest Car Insurance in Florida for Seniors – Actual Rates & Savings

Generic rate tables don’t tell you much. Real savings require real context — your age, your ZIP code, your driving habits. Here’s what Florida senior car insurance actually costs in 2026, broken down honestly.

Short Summary

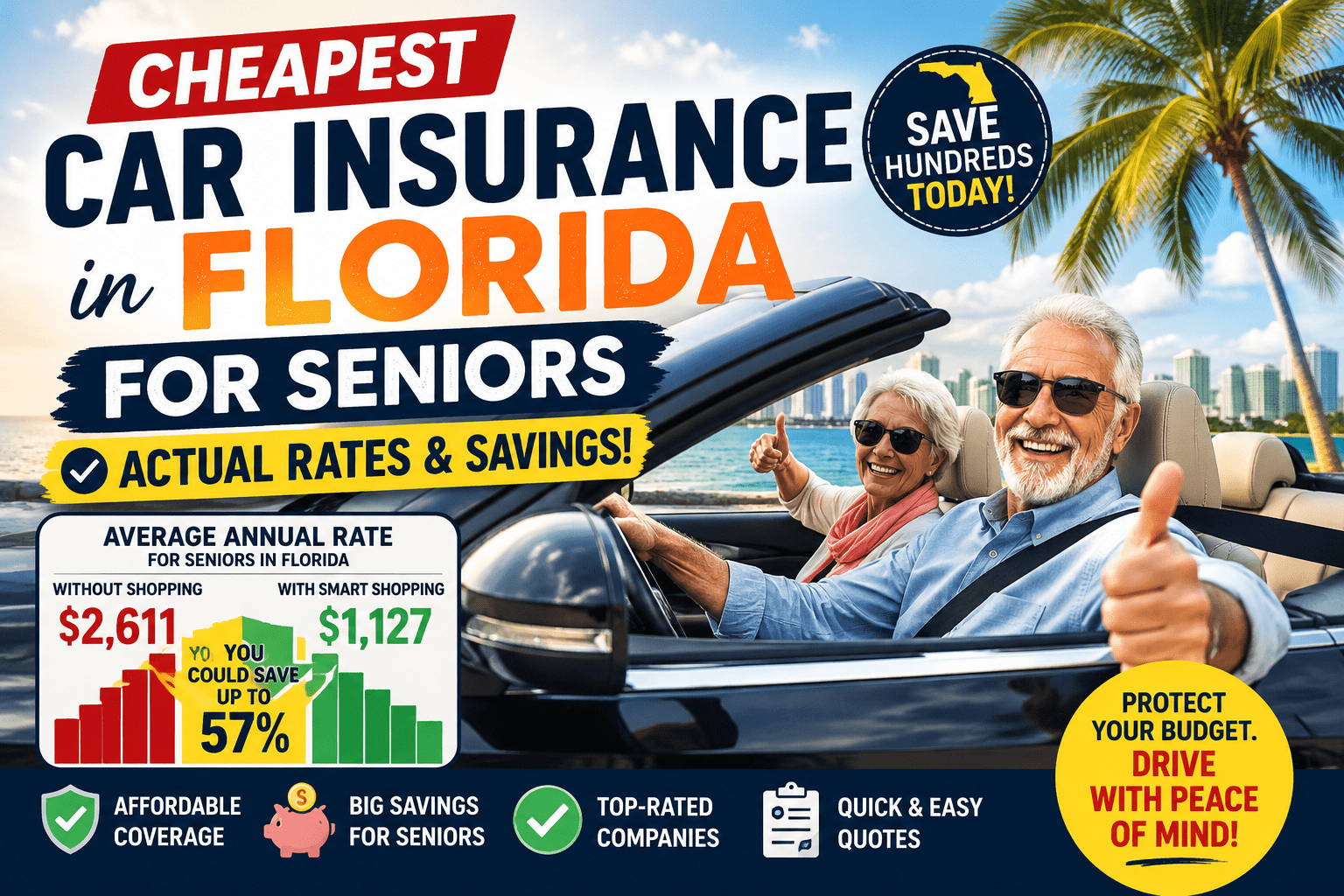

Florida senior car insurance costs vary dramatically by age bracket, ZIP code, carrier, and which discounts are actively applied. A 65-year-old in Gainesville with a clean record can realistically pay under $1,900/year for full coverage with the right carrier and discount stack. A 74-year-old in Miami with one at-fault incident might face $3,800+. This guide breaks down actual rate ranges by region, age bracket, and carrier — and shows exactly how the cheapest options compare once all available senior discounts are applied. The gap between “what you’re paying” and “what you should be paying” is often $800–$1,600 per year.

Why “Cheapest” in Florida Is More Complicated Than It Sounds

The first thing I tell anyone asking about the cheapest car insurance in Florida for seniors is this: cheap and good are not mutually exclusive — but cheap without context is meaningless. A $1,600/year policy from a carrier with a 40% claims dispute rate is not a good deal. A $2,100/year policy from USAA or State Farm with clean claims handling and three stacked discounts is genuinely cheap for what you’re getting.

What I want to do in this guide is give you actual rate ranges that reflect what Florida seniors are realistically paying in 2026 — not the idealized figures that assume perfect credit, zero incidents, and optimal ZIP codes. Then I’ll show you the specific steps that turn a high rate into a competitive one.

I recently helped a 71-year-old named Gene from Clearwater who had been told by two different people that his $3,240 annual premium was “pretty typical for his age and area.” It wasn’t. After walking through the process I describe below, Gene switched carriers and his annual cost dropped to $2,010. The work took about 90 minutes and a $20 AARP course fee.

For the full discount-stacking strategy behind results like Gene’s, see our comprehensive guide: The Car Insurance Secret Florida Seniors Are Using to Save Thousands.

What Factors Affect Your Rate Most as a Florida Senior?

Before looking at numbers, it’s worth understanding the variables that move your rate most significantly. This helps you identify which factors you can influence and which are fixed.

The key takeaway: while you can’t change your age or your ZIP code, you can control your carrier selection, your reported mileage, your course completion status, and your bundling strategy. Together, these controllable factors can offset most of the fixed-cost drivers.

What Does Car Insurance Actually Cost for Florida Seniors by Region?

Florida is not one insurance market. It’s several markets with dramatically different cost profiles. Here’s how the geography breaks down for a representative senior profile (68 years old, clean record, full coverage, 7,500 miles/year):

*Regional estimates based on representative senior profile with clean record. Actual rates vary by specific ZIP code, vehicle, coverage levels, credit score, and individual insurer pricing. Miami-Dade in particular can vary widely by specific neighborhood.

My observation: The regional variation in Florida is dramatic enough that a senior in Gainesville and a senior in Miami with identical profiles can face a $1,400–$2,000 annual cost difference just based on geography. If you’re planning a move within Florida, the insurance cost differential is absolutely worth factoring into your decision — it can be more significant than many people realize.

Which Carrier Is Cheapest for Florida Seniors After All Discounts Are Applied?

This is the right question — not “which carrier has the lowest base rate” but “which carrier is cheapest after applying every discount I qualify for.” Those are often very different answers.

Here’s what realistic all-in annual rates look like for a representative senior (68, clean record, Central Florida, full coverage, 7,500 mi/year) after mature driver course discount, low-mileage discount, and any bundling discount are applied:

*USAA: military/veteran eligibility required. All figures are estimates for representative Central Florida senior profile; actual rates will vary. Discounts calculated at 10% mature driver, 15% low-mileage, and 20% bundle (where applicable). GEICO does not typically offer home insurance bundling directly; their auto rate stands on its own.

The lesson from this table: Travelers looks expensive at the base rate but becomes highly competitive for homeowners who bundle. GEICO’s strong discount structure makes their all-in rate one of the best for non-bundlers. And State Farm hits an excellent balance for those who want competitive pricing with a local agent relationship.

How Much Can Florida Seniors Realistically Expect to Save?

Based on everything I’ve seen helping Florida seniors navigate this process, here’s a realistic savings projection by action taken:

How Do You Actually Get the Cheapest Rate? A Practical Step-by-Step Guide

Here’s the exact sequence I walk seniors through when the goal is finding the lowest possible rate with solid coverage:

- Pull your current declarations page. Know your exact coverage levels and current annual premium. This is your benchmark.

- Check your current rated mileage. Call your insurer and ask: “What annual mileage am I currently rated at?” If it’s over 10,000 and you’re retired, it may be outdated.

- Complete the AARP Smart Driver course if not done in the last 3 years. Download the certificate the moment you finish.

- Get at least 3 direct quotes from USAA (if eligible), State Farm, and GEICO with your corrected mileage and the mature driver discount explicitly applied.

- If you’re a homeowner, add Travelers to your comparison and ask for bundled home + auto pricing from State Farm as well.

- Ask about telematics programs from each carrier (Drive Safe & Save, Snapshot, Drivewise). If your driving is gentle and infrequent, these can add significant additional savings.

- Compare the total annual cost with the same coverage levels across all quotes. Ensure you’re comparing identical deductibles and liability limits.

- If the savings are $400 or more per year, make the switch. Set a new policy start date that overlaps with your current cancellation date by one day.

- Mark your calendar 9 months from now to repeat this process before your next renewal.

Gene’s result from this exact process: 71 years old, Clearwater, 5,900 annual miles. Was paying $3,240. After submitting his (already completed) AARP certificate, correcting his mileage from 12,000 to 5,900, and switching from his longtime insurer to State Farm with Drive Safe & Save enrolled: $2,010/year. That’s $1,230 recovered per year. The entire process took about 90 minutes.

Questions About Getting the Cheapest Car Insurance in Florida as a Senior

Does dropping to minimum liability coverage make it cheaper?

Yes, but at significant risk. Florida’s minimum liability limits (10/20/10) are dangerously low. A serious accident could expose you to personal liability far exceeding those limits. I never recommend going below 100/300/100 for seniors who have assets to protect — and most Florida seniors do. The savings from dropping to minimum limits rarely justify the financial exposure.

Should I drop comprehensive and collision on my older car to save money?

This depends on the vehicle’s current market value. A common guideline: if the annual cost of comprehensive + collision exceeds 10% of the car’s current market value, it may be worth reconsidering. But for vehicles worth $12,000+, which includes most cars from 2017–2022, I generally recommend keeping full coverage — especially in Florida, where a single hurricane or flooding event could total a vehicle.

Is it true that Florida insurance rates are about to change with recent reform bills?

Florida’s insurance regulatory environment has seen significant legislative activity in recent years aimed at reducing litigation abuse and stabilizing the market. The impact on auto insurance rates for seniors specifically is expected to be gradual. The best approach in any regulatory environment: shop at every renewal regardless of what the market is doing, and stack every discount available to you.

Conclusion

The cheapest car insurance in Florida for seniors isn’t a hidden secret. It’s the result of a specific process: finding the most competitive carrier for your exact profile, applying every discount you legally qualify for, and doing that search regularly rather than once and forgetting. The seniors who pay $1,600–$2,100/year in Central Florida are not lucky. They are organized. They submitted their course certificate. They corrected their mileage. They shopped. That’s the entire formula.

You now have the rate data to understand where you should be. You have the steps to get there. The only thing left is starting.