What Is the Average Car Insurance Rate for a 69-Year-Old in Florida? (2026)

Short Summary

The market average for a 69-year-old driver in Florida in 2026 sits between $170 and $210 per month — but that average includes a large proportion of drivers who are overpaying. Drivers who actively optimize their policies through carrier comparison, mature driver discounts, low-mileage rates, and smart deductible choices consistently land well below that range. This article breaks down what drives the average, what separates the overpayers from the well-priced, and how to figure out exactly where your current premium sits on that spectrum.

TL;DR — What Should a 69-Year-Old Actually Expect to Pay for Car Insurance in Florida in 2026?

The short answer: somewhere between $109 and $230 per month, depending on your specific profile and how actively you’ve managed your policy. That’s a wide range — and it’s intentional. The spread between the best-optimized rate and the passive-renewal rate for an identical 69-year-old driver in Florida can genuinely exceed $100 per month.

I want to be direct about what “average” means here. When insurance research sites publish average rates for seniors in Florida, they’re taking the mean across all policyholders in that age and state bracket — the people who shopped carefully and the people who haven’t opened their renewal notice in seven years. That average is not a benchmark for good pricing. It’s a description of the market as-is, and the market as-is includes an enormous amount of unnecessary overpaying.

The more useful question isn’t “what does the average 69-year-old pay?” It’s “what should a well-managed policy for a 69-year-old cost?” Those are different questions, and this article answers both.

Rate Ranges at a Glance — 69-Year-Old Driver, Florida, 2026

Passive Renewal

$210+

Never compared the market

Market Average

$170–$195

Occasional shopping, some discounts

Well-Optimized

$109–$150

Active shopping + all discounts applied

Why Do Two 69-Year-Olds in Florida Pay Such Different Amounts for Car Insurance?

This is the question that gets to the heart of the matter. Age is a pricing factor, but it’s one of many — and for drivers who understand the other factors, age’s impact can be substantially offset.

Let me give you a real example. Two 69-year-old women, both in the Tampa area, both driving similar mid-size sedans, both with clean records. One is paying $228/month. The other is paying $127/month. What explains the $101 difference?

- The first has been with the same carrier for 14 years and auto-renews every year

- The second compared quotes last spring and switched to a better-priced carrier

- The first never completed the mature driver course — the discount was never applied

- The second completed it two years ago and has a 10% discount locked in

- The first drives about 6,200 miles a year but is rated at the standard 12,000-mile assumption

- The second disclosed her actual mileage and is on a low-mileage rate

Same age, same state, same risk profile. Completely different premiums — entirely because of how actively each person manages her policy. That gap is not random. It’s predictable, and it’s fixable.

My experience: The single most reliable predictor of whether a senior is overpaying for car insurance isn’t their age, their vehicle, or their driving record. It’s whether they’ve shopped the market in the last 12 months. That variable alone explains more of the rate variance I see than almost anything else.

What Do the Numbers Actually Look Like? A Detailed Rate Breakdown for 69-Year-Old Florida Drivers

Let me put the rate data in structured context. These tables reflect 2026 market estimates for a 69-year-old Florida driver with a clean record and a standard mid-size vehicle.

Table 1: Average Monthly Rates by Coverage Level — 69-Year-Old, Florida, Clean Record

Table 2: Key Variables That Move the Rate Up or Down for a 69-Year-Old in Florida

Table 3: How a 69-Year-Old’s Rate Compares Across Florida’s Major Metro Areas

Note: Metro-level estimates based on market patterns. Significant within-metro variation exists based on ZIP code, vehicle type, and individual profile.

How Do You Get Below the Average? A 6-Step Process for 69-Year-Old Florida Drivers

The average is a description of the market. These steps are how you beat it.

Know What You’re Currently Paying — and What You’re Getting For It

Pull your current declarations page right now. What’s your monthly premium? What are your liability limits, your deductibles, and which discounts are currently applied? Most people I speak with can tell me their monthly payment but can’t tell me a single coverage limit on their policy. That information gap is expensive.

My advice: If you don’t have a physical or digital copy of your declarations page, call your insurer and ask them to send it to you today. You cannot intelligently compare your policy against the market without knowing precisely what you have.

Benchmark Your Current Rate Against the Tables Above

Look at the tables in this article. Where does your current premium fall relative to the “passive renewal average,” the “market average,” and the “optimized rate” columns? If you’re in the passive renewal column — and especially if you’ve been with the same carrier for more than five years without shopping — you have significant room to move.

Be honest with yourself about where you fall. The benchmarks are ranges, not guarantees. Your specific profile may place you higher or lower than the averages. But the benchmark tells you whether further investigation is worth your time.

Identify Every Discount You Qualify For Before Getting a Single Quote

Make a list before you go to market. At 69, you likely qualify for: mature driver discount (with course certificate), low-mileage discount (if under 7,500 miles/year), multi-policy discount (if you bundle with home/renters), pay-in-full discount, and potentially a preferred credit tier rate if your score is 720+.

If I were in your shoes: I’d complete the mature driver course before getting any quotes. That certificate is worth 5–12% off your premium and it takes a weekend to get. Walk into every quote conversation with it in hand — it changes the numbers from day one.

Get Five Quotes — and Make Each One Work for Your Specific Profile

Use two comparison platforms to capture a wider range of carriers. When entering your information, be precise: your actual annual mileage, your credit tier, your Medicare status, and the mature driver certificate. These details move the needle. A generic quote without this personalization is not a useful data point.

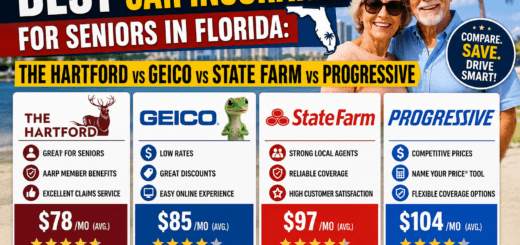

Also call at least one carrier directly — particularly AARP/The Hartford if you’re an AARP member. Some discounts and rate structures are only surfaced through a direct conversation with a licensed agent, not through automated quote tools.

Run the Deductible Math Before Choosing a Policy

For each quote that interests you, calculate the monthly saving from raising your deductible by $500 or $1,000. Divide the increased deductible by the monthly saving to find your break-even period in months. If your clean-record history exceeds that break-even period, the higher deductible is almost always the better financial choice.

Example: Raising your deductible from $500 to $1,500 saves $31/month. The deductible increase is $1,000. Break-even: 32 months. If you haven’t had a claim in the last 32 months — and most careful 69-year-old drivers haven’t — you’ve already passed the break-even point in your previous policy’s lifetime.

Switch or Negotiate — and Lock In an Annual Review Habit

If a better quote exists — switch. If you’d prefer to stay with your current carrier, use the best competing quote as leverage. Call them, tell them what you’ve found, and ask if they’ll compete. Then, regardless of what you decide this year, set a calendar reminder for 11 months from now. The rate environment changes. Your vehicle’s value changes. Your age bracket will tick up. Annual review is not optional — it’s how you stay below the average instead of drifting back toward it.

My experience: The seniors I know who consistently pay well-optimized rates aren’t doing anything complicated. They just never auto-renew passively. That one habit — annual comparison, annual renegotiation — is worth more than any single discount or coverage tweak.

What Does “Below the Average” Actually Look Like in Real Life?

Dorothy is 69 years old. Tampa. Retired schoolteacher. 2017 Toyota Camry. Clean record. Drives about 5,500 miles a year. Before she worked through this process, she was paying $241/month — well above the passive renewal average for her profile.

After comparing five quotes, claiming her mature driver discount, disclosing her actual mileage, raising her deductible, and switching carriers, she landed at $109/month — firmly in the optimized range. The full story of exactly how she got there, with the carrier comparison table and step-by-step breakdown, is in the main case study linked below.

Dorothy’s Result vs. the Averages

69-year-old, Tampa, full coverage, 2017 Camry

Was paying

$241/mo

Now pays

$109/mo

Annual saving

$1,584

Read the Full Case Study

The complete breakdown — every step Dorothy took, the five-carrier comparison table, and the exact discounts that moved the needle — is in the main article.

Objections Answered — “My Situation Is Too Complicated for These Averages to Apply”

❓ “My rate is already around $170. Am I really overpaying or is that acceptable?”

$170 is within the market average range, so you’re not dramatically overpaying by typical standards. But “typical” is the ceiling here, not the goal. With full discount optimization, your target should be $120–$145 for a similar profile. Whether closing that gap is worth 90 minutes of your time is a judgment call — but at $30–$50/month, the math is usually clear.

My advice: Even if you’re at $170, get quotes. If nothing better comes back, you’ve confirmed your rate is fair and you can auto-renew confidently this year. That confirmation has value too.

❓ “I live in Miami. Are these averages even relevant to me?”

The table above shows Miami/Fort Lauderdale running about 29% above the state average. That’s real, and it means your starting baseline is higher. But the optimization levers still apply — and they’re worth proportionally more in a high-cost market. At $248/month, a 10% mature driver discount is worth $298/year. Same percentage, more dollars. The effort-to-reward ratio is actually better in high-cost markets.

❓ “I had an accident three years ago. Do these averages still apply to me?”

Your rate will be higher than these averages — but how much higher depends on the carrier. Different insurers penalize accidents over three years old very differently. Some have already largely forgiven it; others continue to rate you on it for five years. This variance is exactly why comparing multiple carriers is essential for anyone with any blemish on their record. Don’t assume a single high quote represents the market.

❓ “I’m almost 70. Should I expect a big rate jump soon?”

Many carriers apply a rating step-up at age 70, yes. The magnitude varies by carrier — some are sharp, some are modest. The strategic response is to shop the market in the 3–6 months before you turn 70, specifically looking for carriers whose underwriting model treats the 70+ bracket more generously. Locking in a new policy before you cross that threshold can effectively delay the age-70 surcharge by a year or more, depending on your renewal cycle.

How Do You Get Your Own Accurate Quote and See Where You Stand?

Here’s the condensed, actionable version — what to do this week.

Pull your declarations page. Know your exact current premium, limits, and deductibles. Compare against Table 1 above to benchmark where you are.

Complete your mature driver course. Enroll online through AARP or a Florida-approved provider. Get your certificate before quoting.

Get five optimized quotes using two platforms. Disclose your certificate, mileage, credit score. Ask about every applicable discount explicitly.

Run deductible scenarios on your top two quotes. Decide whether a higher deductible is appropriate given your history.

Switch or negotiate. Confirm new policy active. Cancel old policy. Set annual review reminder. Done.

Frequently Asked Questions

What is the average monthly car insurance rate for a 69-year-old in Florida with a clean record?

In 2026, the market average for a 69-year-old Florida driver with a clean record and full coverage sits between $170 and $210 per month. This average includes both optimized and unoptimized policies. Drivers who actively shop, apply available discounts, and adjust their coverage structure consistently land between $109 and $150 per month for comparable coverage.

How much more does a 69-year-old pay compared to a 50-year-old for the same coverage in Florida?

On average, 15–25% more, depending on the carrier and coverage type. The gap begins widening noticeably from age 65 and accelerates at 70. However, this age surcharge is partially offset-able through mature driver discounts, low-mileage rates, and carrier selection. The best-priced 69-year-old can pay less than the worst-priced 50-year-old.

Does where you live in Florida significantly affect car insurance rates for seniors?

Yes — substantially. South Florida (Miami, Fort Lauderdale, West Palm Beach) runs 25–30% above the state average due to PIP fraud exposure, litigation culture, and traffic density. North Florida and smaller metro areas like Gainesville and Tallahassee can run 15–20% below average. If you’re in a high-cost area, this makes the savings from active policy management even more valuable in absolute dollar terms.

Is $109 per month for a 69-year-old in Florida realistic, or was Dorothy’s case an exception?

It’s realistic for a driver with a clean record, good credit, low annual mileage, and a vehicle in the $12,000–$18,000 range who has applied all available discounts and is with a carrier that prices her profile favorably. It’s not achievable for every 69-year-old in Florida — drivers in high-cost ZIP codes, with recent claims, or with lower credit scores will have a higher floor. But $109 is not anomalous — it’s the result of systematic optimization by a driver who fit the profile.

What is the cheapest car insurance option for a senior in Florida who drives very little?

For very low-mileage seniors — under 5,000 miles per year — usage-based or pay-per-mile insurance programs can offer the lowest available rates. Carriers with telematics programs that track your actual driving reward calm, low-frequency drivers heavily. For seniors who rarely drive highway speeds, brake gently, and drive during low-risk hours, these programs can produce savings of 20–30% versus standard policies.

How long does it realistically take to find a better car insurance rate as a senior in Florida?

The full process — from pulling your current declarations page to binding a new policy — takes most seniors between 90 minutes and three hours spread over a week. This includes completing the mature driver course (4–6 hours online, often done in two sessions), getting five quotes (45–60 minutes), comparing options (30 minutes), and completing the switch (20–30 minutes). The total time investment, against potential annual savings of $600–$1,500, represents one of the highest-value uses of a few hours most seniors can make.