Car Insurance Rates in 2026: What’s Driving the Surge and Who’s Hit Hardest

Short Summary

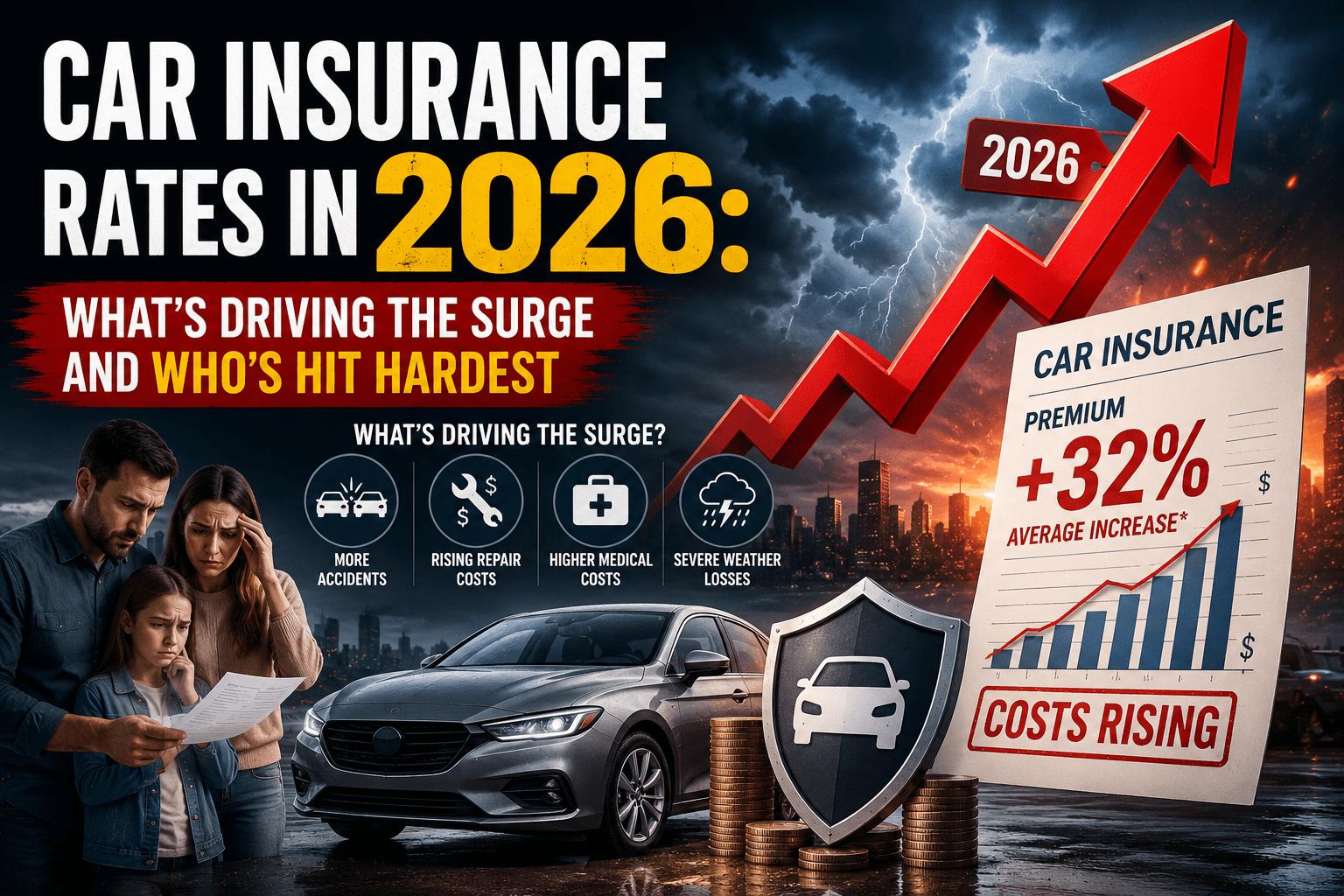

Car insurance rates in 2026 have reached levels that would have seemed extraordinary just four years ago. The national average for full-coverage auto insurance now sits at roughly $2,100 per year — up more than 40% since 2021. Senior drivers are absorbing the sharpest end of those increases, with drivers over 70 facing average premiums that have nearly doubled in five years. This guide dissects every factor driving the 2026 rate environment, presents the data by driver segment and state, and lays out the complete strategy I used to cut my own premium against the trend.

TL;DR – Quick Summary

- The national average full-coverage auto insurance rate in 2026 is approximately $2,100/year — a 40%+ increase since 2021.

- Senior drivers over 70 face average premiums of $2,400–$2,900, with some high-cost states exceeding $3,500.

- The primary drivers are vehicle repair inflation, litigation explosion, reinsurance cost surge, and insurer loss-ratio recovery.

- Not all states, carriers, or driver profiles are hit equally — the spread between best and worst case for a given driver can exceed $1,000 per year.

- Active shoppers — those who compare quotes annually and stack discounts — consistently pay 18–35% below the market average for their profile.

What Are Car Insurance Rates Actually Doing in 2026 — and How Did We Get Here?

THE STATE OF THE MARKET

I track my insurance costs the way I track my utility bills and grocery spending — every year, every renewal, every line item. I have been doing this since 2014. And I can tell you from direct, personal observation that the 2024–2026 period represents the most significant and sustained premium surge I have seen in twelve years of careful tracking.

My own full-coverage premium crossed $2,000 for the first time in 2024. It hit $2,280 in 2025 before I intervened. By the time I finished shopping, stacking discounts, and switching carriers in early 2026, I had brought it back to $1,520. But the point is that without that intervention, the trajectory was vertical — and I had done nothing to cause it.

To understand 2026’s rate environment, you need to understand the cascade of events that built up over five years. Each event fed into the next. Each cost increase was passed on to policyholders. And the cumulative result is what your renewal notice is reflecting right now.

When did the current rate cycle actually begin?

The current cycle began in earnest in mid-2022. Prior to that, auto insurance premiums had been artificially suppressed by several years of underpricing as insurers competed aggressively for market share. Driving patterns also shifted during the pandemic — fewer miles driven temporarily reduced claims, and some insurers passed this along as temporary refunds. When driving resumed and claims costs accelerated, the gap between what insurers were charging and what they were paying out became untenable. The correction began in 2022 and has continued uninterrupted through 2026.

Is the 2026 rate surge happening equally across all states?

Absolutely not. State regulation, litigation environment, weather exposure, and carrier competition vary enormously. Florida, Michigan, Louisiana, and California consistently rank among the most expensive states for auto insurance. Maine, Ohio, and Vermont are among the least expensive. The same driver with the same car and record can pay dramatically different premiums depending simply on their state of residence.

⚡ My Experience

In late 2025, I moved from suburban Illinois to a comparable suburb in Indiana — largely for family reasons, but with full awareness that Indiana has meaningfully lower insurance rates. My premium dropped $340 per year for identical coverage and identical driving behavior. The ZIP code was the entire explanation. This is not a practical recommendation for most people, but it illustrates how large the geographic variable actually is in the 2026 rate environment.

What Are Average Car Insurance Rates in 2026 — By State, Age, and Profile?

THE DATA — PRESENTED CLEARLY

Let me present the numbers in two layers: first by driver age group (national averages), and then a state-by-state comparison for senior drivers specifically. Together, these tables paint a complete picture of where you stand relative to the market.

Table 1 — National Average Full-Coverage Premium by Driver Age (2026)

National estimates for full coverage, single vehicle, clean record. Actual rates vary significantly by state, carrier, ZIP code, and individual risk profile.

Table 2 — Average Senior (Age 70) Annual Premium by State — 2026 (Top 10 Most & Least Expensive)

Estimated averages. Individual rates vary by ZIP code, carrier, vehicle, and driving record. Use these as benchmarks, not guarantees.

💡 My Recommendation

If you live in Florida, Michigan, or Louisiana and are over 65, you are in the worst possible intersection of state-level rates and age-band pricing. Your most powerful lever in those states is aggressive carrier shopping — because the spread between the highest and lowest quote for the same coverage is enormous in high-cost states. Do not settle for the first quote. Carriers price those markets very differently from each other, and the difference between them is often $600–$900 per year for a senior driver.

What Are the Real Forces Behind the 2026 Car Insurance Rate Surge?

BEHIND THE NUMBERS

Insurance companies issue one-sentence explanations for rate increases that explain essentially nothing. “Market conditions.” “Loss cost adjustments.” “Reinsurance factors.” These phrases are accurate but empty of meaning for the average policyholder. Let me translate them.

How much has vehicle repair actually contributed to higher rates?

More than most people realize. The average cost to repair a front bumper on a vehicle equipped with ADAS (advanced driver assistance systems) sensors now runs $3,200–$4,800 compared to $800–$1,200 on a vehicle without sensors. A door mirror with integrated camera and blind-spot monitoring costs $900–$1,400 to replace. A windshield with embedded rain and light sensors: $1,100–$1,800. Modern vehicles are extraordinarily expensive to repair after even minor collisions, and the trained technicians to perform that work are in short supply.

Nationally, the average auto collision claim payout has increased approximately 44% since 2020. That increase flows directly into collision and comprehensive premiums — and there is no technical solution on the near horizon that reverses this trend.

What role has the legal environment played in driving 2026 rates?

A substantial one. The rise of litigation finance — where outside investors fund plaintiffs’ legal cases in exchange for a portion of settlements — has changed the economics of auto accident litigation fundamentally. Cases that previously settled quickly and modestly now proceed to trial more frequently, with higher settlement expectations built in from the start. “Nuclear verdicts” (jury awards over $10 million in auto liability cases) tripled between 2021 and 2025. Insurers build these expected payouts into reserves — and those reserves are funded through your premium.

What is the reinsurance factor — and why does it matter to you?

Reinsurance is insurance for insurance companies. Carriers buy reinsurance policies to protect themselves from catastrophic loss events — major weather disasters, multiple large claims in a short period, and so on. After several years of historically large weather-related auto losses (hailstorms destroying parked vehicles, flooding, wildfires), global reinsurers raised their rates sharply. Between 2022 and 2025, property-casualty reinsurance costs rose approximately 40%. That increase was passed through to auto policyholders in the form of higher premiums — even in areas where those weather events never happened.

How Can You Beat the 2026 Rate Environment — A Complete Step-by-Step Strategy?

THE COUNTER-STRATEGY THAT WORKED FOR ME

I am going to lay this out exactly as I executed it — not as a theoretical framework but as the actual sequence I followed over five months in late 2025 and early 2026. By the time I finished, my premium was $760 per year lower than it had been at peak, despite being a year older and in a market that continued rising. Here is the sequence.

What Are the Most Pressing Questions About Car Insurance Rates in 2026?

HONEST ANSWERS TO THE QUESTIONS PEOPLE ACTUALLY HAVE

What Does the 2026 Rate Environment Mean for You — and What Should You Do Next?

THE BOTTOM LINE

The data in this article should do two things. First, it should make clear that the increases you are seeing are real, systemic, and not going away on their own. There is no cavalry coming. Rates are not going to reset. The market has permanently repriced.

Second, and equally important, the data should make clear that the spread between what passive auto-renewers pay and what active shoppers pay has never been wider. If you do nothing, you will pay the market maximum for your profile. If you follow the steps I have outlined — in the order I have outlined them — you will consistently pay well below it.

I am 71 years old. I live on a fixed income. I drive a 2020 Honda CR-V approximately 5,900 miles per year. I have a clean record and a strong credit score. My annual full-coverage premium in 2026 is $1,475. The market average for my profile and state is approximately $2,200. I am paying $725 per year less than average — not through any special access or expertise, but simply by doing the work that most people skip.

⭐ If I Were In Your Shoes — My Exact Priority Order

- Today: Pull your declarations page. Read every line. Flag every coverage you cannot immediately justify.

- This week: Call insurer. Report actual mileage. Ask for all currently applied discounts and any eligible-but-unapplied ones.

- This month: Complete or renew a defensive driving course. Submit the certificate directly — do not wait for them to find it.

- Next 30 days: Get at least four competing quotes. Use identical coverage levels. Include Amica and USAA (if eligible).

- Before renewal: Evaluate collision coverage math on older vehicles. Raise deductibles if emergency savings support it.

- Decision time: If a competing carrier offers $200+ in annual savings with comparable strength ratings, switch. Do not let loyalty cost you money that nobody is rewarding you for.

- Year 2 and beyond: Set a calendar reminder 45 days before renewal. Repeat. The second time takes 90 minutes. The savings compound.

The 2026 car insurance rate environment is genuinely challenging. But it is not hopeless, and you are not powerless. The tools I have described are available to every driver who chooses to use them. The only question is whether you will.