Cheap Full Coverage Car Insurance for Seniors in Florida – What You Should Actually Buy

Most articles tell you to “keep full coverage” without explaining what it actually costs you — and when it becomes a waste of money. I’ll be more honest than that.

📋 Short Summary

Full coverage for Florida seniors in 2026 costs anywhere from $140 to $230+ per month depending on your car, location, and carrier. Whether you should pay for it depends entirely on your vehicle’s current value, your deductible, and your financial cushion. This guide explains exactly what “full coverage” includes (and what it doesn’t), when it makes financial sense to keep it, when to drop collision but keep comprehensive, and how to find the cheapest full coverage options for elderly drivers in Florida.

What Does “Full Coverage” Car Insurance Actually Mean in Florida?

Here’s something that surprises a lot of people: there’s no official insurance policy called “full coverage.” It’s an informal term that generally means you’re carrying liability + collision + comprehensive. But what exactly each of those covers — and what gaps remain even with “full coverage” — matters enormously, especially in Florida.

The Florida-specific reality: Even “full coverage” doesn’t make you whole against every risk. Florida has no fault insurance laws, a 20%+ uninsured driver rate, and catastrophic weather risks. You need comprehensive for the weather, UM/UIM for uninsured drivers, and bodily injury liability to protect your retirement savings. All of this needs to be in your policy — not just the collision and comprehensive that most people associate with “full coverage.”

This is part of our broader series. For a complete overview of all your options, visit our main guide on car insurance for Florida seniors in 2026.

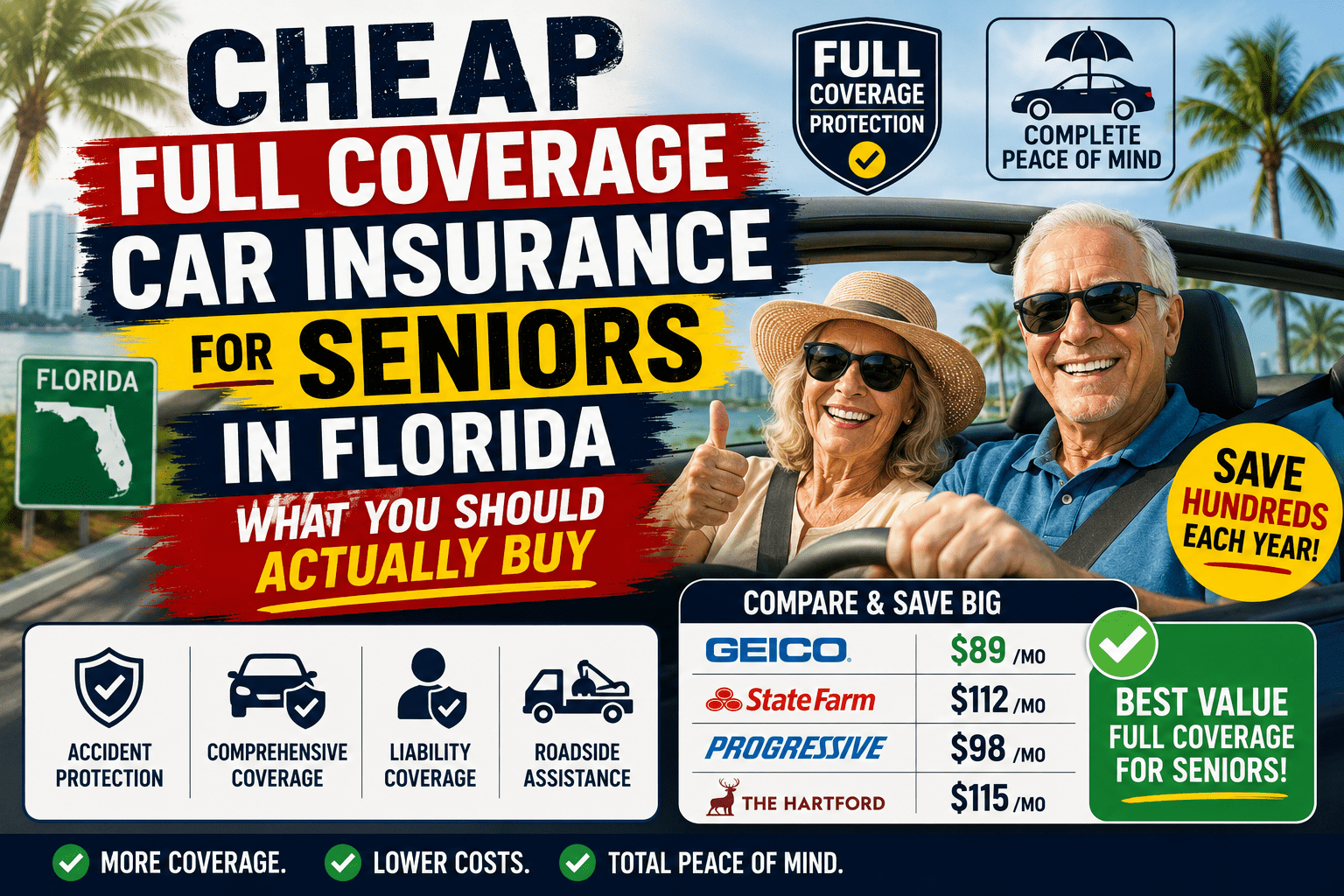

How Much Does Full Coverage Car Insurance Cost for Elderly Drivers in Florida?

I pulled full-coverage-specific quotes in early 2026 for a range of senior profiles. Here’s what full coverage (liability + collision + comprehensive + UM) actually costs:

“Without Collision” column = liability + comprehensive + UM only, Hartford pricing. Rates vary by specific ZIP and driver profile.

Look at that last column. Dropping collision saves $53–$65/month in most of these profiles. For a 2015 Ford Escape worth $9,000, that’s paying $636–$780 per year for collision coverage that would pay out a maximum of $8,000 (minus your deductible). The math deserves scrutiny.

When Should Florida Seniors Keep Full Coverage — and When Should They Drop Collision?

This is the question I get most often, and the answer is genuinely different for different people. Let me lay out the decision framework I use:

The Full Coverage Decision Calculator

Ask yourself these three questions:

1. What is my car worth today? (Check KBB.com)

- Under $8,000 → Strongly consider dropping collision

- $8,000–$14,000 → Borderline; run the annual cost calculation below

- Over $14,000 → Keep full coverage

2. What is my annual collision + comprehensive premium?

- If your annual collision premium exceeds 10% of your car’s market value → it’s likely not worth keeping

- Example: Car worth $8,000. Collision costs $540/year. 540/8000 = 6.75% — borderline but probably worth keeping

- Example: Car worth $6,000. Collision costs $600/year. 600/6000 = 10% — time to seriously consider dropping it

3. Could I absorb the cost of replacing or repairing my car out of pocket?

- If yes → dropping collision is a reasonable bet

- If no → keep collision regardless of the math, because the risk is catastrophic for your budget

⚠️ Florida Exception: Always Keep Comprehensive

Even if you drop collision, do NOT drop comprehensive in Florida. Comprehensive covers hurricanes, flooding, hail, and sinkholes — all real risks in this state. Comprehensive is also cheap relative to collision (often $30–$50/month for the coverage it provides). A Category 3 hurricane can total a car parked in a driveway. This is not a theoretical risk in Florida — it’s a regular occurrence.

My Real Experience: The Case of the Overinsured Buick

A retired couple I know in Sarasota — both in their mid-70s — had a 2013 Buick Enclave. Great car in its day, but Kelley Blue Book in early 2026 put it at about $7,800. They were paying $214/month for full coverage, including collision at a $500 deductible.

Their collision premium alone was $74/month — that’s $888 per year. For a car worth $7,800 with a $500 deductible, the maximum they’d ever collect from a total loss claim was $7,300. They’d need to file a significant total-loss claim within roughly 8.2 years just to break even on those premiums — and statistically, most cars don’t get totaled.

We dropped collision, kept comprehensive (for the hurricane/flood risk), and raised their bodily injury and UM limits. New monthly premium: $158.

They saved $672/year and actually had better liability protection than before.

⚡ If you’re in a similar situation… Pull out your policy and look at what you’re paying specifically for collision. Then look up your car’s current value. If those two numbers don’t make sense together, you’re probably paying for coverage that won’t serve you as well as you think.

How Can Florida Seniors Get the Cheapest Possible Full Coverage in 2026?

If your vehicle and situation justify keeping full coverage, here’s how to pay as little as possible for it:

Raise your deductibles

Going from $500 to $1,000 on both collision and comprehensive typically reduces your premium by 15–22%. If you have $1,000–$1,500 in savings you could access in an emergency, this is often the right call. The annual savings over 3–4 years usually exceed the extra deductible amount.

Get a quote with AARP + Hartford

For full coverage specifically, The Hartford AARP program consistently comes in 10–18% lower than Allstate and 6–12% lower than State Farm. It’s the most impactful single action most Florida seniors can take.

Take the AARP Smart Driver course before quoting

Completing an approved defensive driving course before getting quotes means those discounts are already baked in when you compare. Don’t get a quote and then take the course — you lose the full comparison value.

Bundle home and auto

For full coverage policies specifically, bundling tends to yield larger percentage discounts because the combined premiums are higher. A 12% bundle discount on a $200/month policy saves $24/month — $288/year.

Remove unnecessary add-ons from your existing policy

Roadside assistance, rental car reimbursement, and gap insurance are all potentially redundant if you have AAA membership, a second car, or a paid-off vehicle. Strip add-ons you’re duplicating elsewhere and you can save $15–$30/month without reducing meaningful coverage.

Frequently Asked Questions: Full Coverage for Florida Senior Drivers

Does full coverage mean I’m covered for everything?

No. “Full coverage” is a marketing phrase, not a legal term. Even with full coverage, you can still face uninsured motorist gaps (if you don’t carry UM), medical payment gaps, rental car costs, and out-of-pocket deductibles. In Florida especially, you need to explicitly verify that uninsured motorist coverage and adequate bodily injury liability are included — these aren’t automatically part of a “full coverage” quote.

My lender requires full coverage — what does that actually mean?

If you’re still making car payments, your lender will require collision and comprehensive coverage. Once your car is paid off, that requirement disappears and the full coverage decision is entirely yours. Many seniors keep paying for full coverage on a paid-off car out of habit — if that’s your situation, reassess now.

What happens if I drop collision and then have an accident that’s my fault?

You pay out of pocket to repair or replace your vehicle. No reimbursement from your insurer for your own car’s damage. The other driver’s property damage liability from your policy covers their vehicle. This is the calculated risk you take when dropping collision — which is why it only makes financial sense when the vehicle’s value is low enough that you could absorb that loss.

Is comprehensive alone enough for a low-value car in Florida?

For many Florida seniors, liability + comprehensive + UM is actually the most rational coverage package for a car worth under $10,000. You’re protected against the financial catastrophe of causing injuries or property damage to others, against weather/theft/non-collision events, and against uninsured drivers hitting you. You’ve just removed the collision piece for a car that doesn’t economically justify it.

My Honest Recommendation on Full Coverage for Florida Seniors

🎯 The Bottom Line

- Car under $8k: Drop collision. Keep comprehensive. Boost liability and UM instead.

- Car $8k–$14k: Run the 10% rule. If collision premium exceeds 10% of car value annually, consider dropping it.

- Car over $14k: Keep full coverage. Shop for the cheapest version via Hartford AARP.

- Always in Florida: Comprehensive coverage is non-negotiable regardless of vehicle value.

- Never compromise on: Bodily injury liability ($100k/$300k minimum) and uninsured motorist ($50k+). These protect your financial future.

For more guidance, return to our main series starting with Why Florida Seniors Are Getting Ripped Off on Car Insurance in 2026.

1 Response

[…] ⚡ If I were in your shoes… I’d carry at minimum: $100k property damage liability, $100k/$300k bodily injury, $50k uninsured motorist, and comprehensive — but I’d skip collision if my car is more than 8 years old or worth under $10,000. That configuration typically runs $140–$175/month with the right carrier for a senior in Florida with a clean record. For the full coverage decision guide, visit our full coverage breakdown for Florida seniors. […]