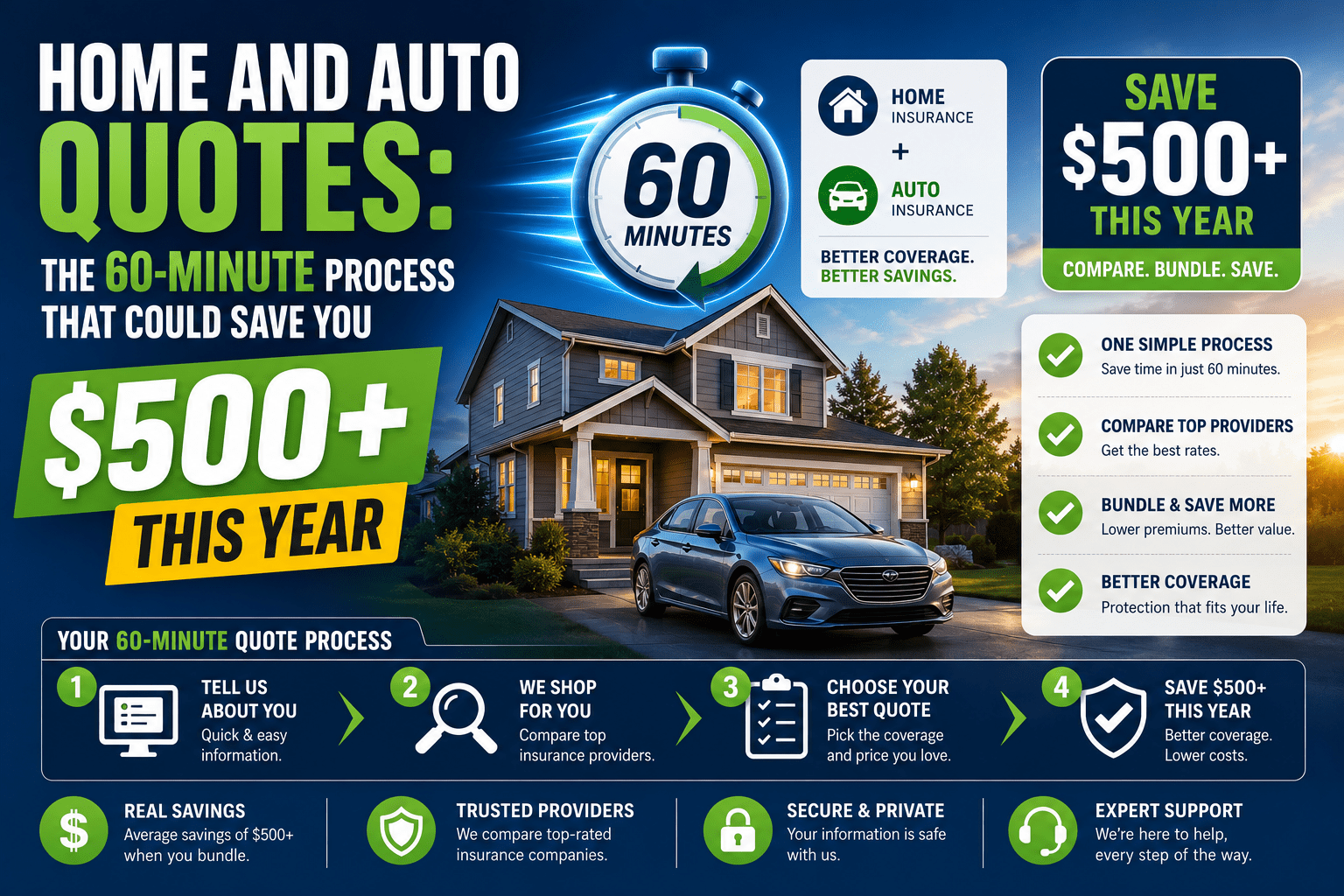

Home and Auto Quotes: The 60-Minute Process That Could Save You $500+ This Year

📋 Short Summary

Shopping for home and auto quotes doesn’t need to consume a weekend. This guide gives you a precise, 60-minute workflow — broken into four distinct phases — that produces accurate, comparable quotes on both policies without the typical runaround. It covers exactly what information you need before you start, which carriers to prioritize, how to use an independent agent to your advantage, what questions to ask on every call, and how to evaluate and act on what you receive. Whether this is the first time you’ve ever shopped your policies or the fifth, this process is the fastest path to a better rate.

⚡ TL;DR – Quick Summary

- Getting accurate home and auto quotes simultaneously is absolutely doable in 60 minutes — with the right preparation.

- The key is gathering all your policy data in advance — 15 minutes of prep produces far better quotes than 3 hours of unprepared calling.

- An independent insurance agent is your single most powerful tool — they shop dozens of carriers simultaneously in one conversation.

- The average household that goes through this process saves $400–$700/year on their combined policies.

- The goal is not just the cheapest number — it’s the best total value across coverage quality, price, and claims reliability.

The Sunday Afternoon That Changed How Much I Pay for Insurance Every Year

It was a rainy Sunday afternoon, and I had nothing urgent on my calendar. On a whim, I decided to finally deal with something I’d been putting off for two years: properly shopping my home and auto insurance. I expected it to take all day. It took 58 minutes.

The first 15 minutes: I pulled both declaration pages, noted every coverage level and deductible, looked up my car’s current value on Kelley Blue Book, and checked my home’s last replacement cost estimate. The next 30 minutes: I called an independent agent who’d been recommended by a friend. He ran quotes from 11 carriers simultaneously while I sat on the phone with him. By the time we hung up, I had a clear winner — a bundled policy with Nationwide that saved me $43/month on auto and $34/month on home. The final 15 minutes: I confirmed coverage details, asked three specific questions, and requested the new binder documents.

That $77/month savings — $924/year — came from 58 minutes of focused work on a rainy Sunday. I still think about that afternoon every time someone tells me they’ve been putting off shopping their policies because “it takes too long.”

💡 My Recommendation: Block 60–90 minutes on your calendar in the next two weeks. That’s all this takes. The prep phase is the key — most people waste hours on calls because they show up unprepared. Gather everything first, then make the calls. You’ll be astonished how efficiently it moves.

What Information Do You Need Before Getting Home and Auto Quotes?

The single most common reason the quote process drags out is showing up to a call without the necessary information. Agents have to pause, you have to go find things, the call gets rescheduled. Spend 15 minutes gathering the following before you make a single call — and every subsequent step becomes dramatically faster.

🏠 For Your Home Insurance Quote

- Year the home was built

- Square footage (living area)

- Construction type (wood frame, brick, concrete block)

- Roof age and material (asphalt, metal, tile)

- Current dwelling coverage amount

- Current personal property coverage amount

- Current liability limit

- Current deductible

- Any home improvements in last 5 years

- Number of claims filed in last 5 years

- Distance to nearest fire station (check your current policy)

- Security system / smoke detector info

🚗 For Your Auto Insurance Quote

- Driver’s license number (all drivers)

- Vehicle VIN (all vehicles)

- Current annual mileage estimate

- Primary use (commute, pleasure, business)

- Current coverage: liability limits, deductibles

- Whether you carry collision and/or comprehensive

- Driving history: any tickets or accidents last 5 years

- Current auto premium (annual)

- Anti-theft devices or safety features in vehicle

- Garaging address (if different from home)

| Information Item | Where to Find It | Time to Gather | Impact on Quote Accuracy |

|---|---|---|---|

| Current policy declarations pages | Insurer portal login | 2 min | Critical |

| Vehicle VIN numbers | Dashboard or title | 1 min | Critical |

| Home year built, sq footage, construction | Property record / Zillow | 3 min | Critical |

| Roof age and material | Purchase records / inspection | 2 min | High |

| Annual mileage estimate | Odometer check | 1 min | High |

| Claims history (both policies, last 5 yr) | Current insurer or CLUE report | 2 min | Critical |

The Exact 60-Minute Home and Auto Quote Process — Phase by Phase

Phase 1: Preparation (0–15 minutes)

The 15 minutes that make the next 45 work

Log into both your home and auto insurer portals. Download both declaration pages. Open your vehicle registration and note the VIN(s). Check Zillow or your county assessor’s website for your home’s basic specs. Write everything on a single sheet of paper or a notes app. When the information is in front of you, every subsequent call takes half the time.

Key output: One organized reference sheet with all policy details for both home and auto.

Phase 2: Independent Agent Call (15–45 minutes)

Your most powerful 30 minutes in this entire process

Call an independent insurance agent — not a captive agent who represents only one carrier. An independent agent represents dozens of carriers simultaneously. In a single 30-minute call, they can run bundled quotes for both your home and auto through 10–15 different carriers at once. This is the highest-efficiency move in the entire quote process. Give them all the information from your Phase 1 reference sheet, specify the exact coverage levels you want to match, and ask them to present both bundle and best-separate options.

During this call, specifically ask: “Can you show me the best bundle total, and also the best separate total if I kept them with different carriers?” Most agents will run both without needing to be asked twice — but ask anyway.

Key output: 3–5 bundled quotes and 2 best-separate totals, all with identical coverage.

Phase 3: Direct Carrier Cross-Check (45–55 minutes)

Verify the winner and check your current insurer

Take the top quote from your independent agent and verify it directly on the carrier’s website or by phone — some carriers offer slightly different rates direct vs. through an agent. Then call your current insurer and tell them you have a competing bundle quote at $X total. Ask them to match or beat it. About 35–40% of the time, they will. If they can’t, you have clear confirmation that switching is the right move.

Key output: Confirmed best quote, verified against direct pricing, and a decision on whether to stay or switch.

Phase 4: Confirm, Finalize, and Switch (55–60 minutes)

The questions to ask before you sign anything

Before confirming, ask your winning carrier three questions: (1) “Are there any other discounts I haven’t been quoted for that I might qualify for?” (2) “What is your average time-to-payment on home and auto claims?” (3) “How does a claim on one policy affect my rate on the other?” Once satisfied, initiate the new policy binders and request a specific start date that ensures zero gap in coverage. Cancel your old policies only after receiving written confirmation that new coverage is active.

Key output: Active new binders on both policies, cancellation notices sent to old carriers, expected refund documented.

🎯 If I Were You… I’d call the independent agent first before anything else — even before looking at online quote tools. A good independent agent will do in 30 minutes what would take you four hours of online quoting to replicate, and they’ll catch discounts and coverage nuances that quote calculators miss entirely. Ask a friend or neighbor for a local agent referral — personal recommendations are consistently the fastest way to find a genuinely skilled one.

What Are the Most Important Questions to Ask When Getting Home and Auto Quotes?

Most people ask only two questions when getting quotes: “How much?” and “What does it cover?” These are necessary but nowhere near sufficient. Here are the questions that actually reveal the quality — and the total value — of what you’re being offered.

| Question to Ask | Why It Matters | Ask For |

|---|---|---|

| “What discounts are included — and are there any I might qualify for that aren’t listed?” | Discounts aren’t automatically applied. This question often unlocks 1–3 additional savings. | Home + Auto |

| “What is your AM Best or S&P financial strength rating?” | Financially weak insurers may struggle to pay large claims. You want A or better. | Both |

| “What does ‘replacement cost’ mean on this homeowners policy — replacement cost value or actual cash value?” | Actual cash value pays depreciated value. Replacement cost pays to rebuild. The difference at claim time can be enormous. | Home |

| “If I file a claim on my home policy, will my auto rate be affected — and vice versa?” | Important to understand cross-policy rate impact before bundling. | Bundle |

| “Does this policy include accident forgiveness for the first at-fault claim?” | Accident forgiveness prevents a rate spike after your first mistake. Worth paying slightly more for. | Auto |

| “What is the cancellation process and will I receive a prorated refund on unused premium?” | Know how to exit cleanly if you find a better rate mid-term. Most policies allow prorated refunds. | Both |

Honest Answers to the Home and Auto Quote Questions People Actually Have

My Final Recommendations: Get Your Home and Auto Quotes Right

01

Spend 15 minutes on preparation before making a single call. That 15 minutes turns a 3-hour ordeal into a 45-minute conversation.

02

Call an independent agent first. One call, dozens of carriers, both policies simultaneously. It’s the single highest-leverage move in the entire process.

03

Always call your current insurer last and present their quote as a match-or-lose scenario. Retention departments have more pricing flexibility than you’d think.

04

Verify claims ratings before you switch. The cheapest policy is only valuable if the insurer reliably pays. Check AM Best, J.D. Power, and NAIC ratios on any new carrier.

Complete Series — Everything You Need to Know About Insurance Quotes

- ← Back to Pillar: Car Insurance Quotes — The Complete Guide

- Senior Car Insurance: The Complete Rate & Discount Guide for Drivers 55+

- Discount Car Insurance Quote: Every Savings Lever, Fully Explained

- Home and Auto Insurance Quote Comparison: Bundle Smarter, Save Bigger

- Car and Homeowners Insurance Quotes: Bundle vs. Separate

- Home and Auto Quotes: The 60-Minute Savings Process