Which Are the Best Car Insurance Companies for Seniors in 2026? (GEICO vs The Hartford vs USAA)

Short Summary

Choosing the best car insurance company as a senior in 2026 isn’t about finding the flashiest ad or the most familiar name — it’s about finding the carrier whose pricing, discount programs, and service model actually match how you drive and what you need at this stage of life. This article compares the top six carriers — The Hartford (AARP), USAA, GEICO, Travelers, Progressive, and State Farm — with an honest head-to-head breakdown of their senior-specific features, 2026 rate estimates, telematics programs, and who each company is genuinely best suited for. Real observations, comparison tables, and a clear framework to help you choose.

I want to be upfront about something before we start: there is no universally “best” car insurance company for seniors. Anyone who tells you otherwise is either simplifying to the point of uselessness or selling something. The right company depends on where you live, what you drive, your claims history, how many miles you put on annually, and whether you qualify for special programs like AARP membership or military service.

What I can give you is an honest, experience-based comparison of the major carriers — built from going through these companies many times with real senior drivers. Some of my takes might surprise you. I’ll tell you who each company is genuinely good for, and I’ll tell you the situations where they fall short.

I’ll also tie each section back to the broader discount strategy that makes a real difference regardless of which company you’re with. Before you lock in any decision, make sure you’ve read the complete savings framework in our pillar guide: The One Car Insurance Trick Most Seniors Don’t Know About in 2026.

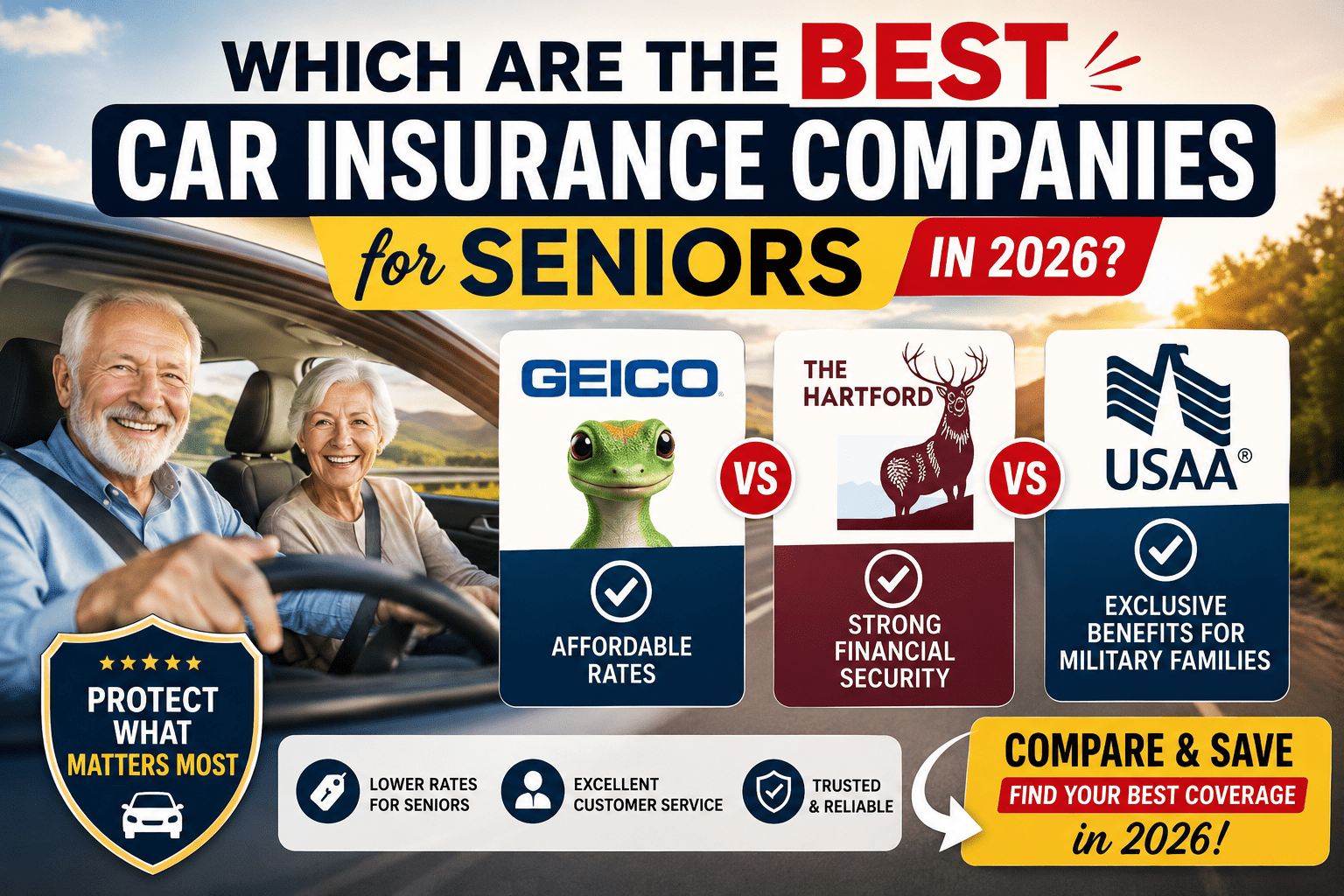

How Do the Top Car Insurance Companies for Seniors Compare Side-by-Side in 2026?

Here’s the full head-to-head overview of the six major carriers most relevant to drivers over 65. I’ve included estimated annual rates, senior discount depth, telematics availability, and claims experience:

| Company | Est. Avg Annual Rate (65+) | Senior Discounts | Telematics Program | Claims Satisfaction | Best For |

|---|---|---|---|---|---|

| The Hartford (AARP) | $1,100–$1,450 | ⭐⭐⭐⭐⭐ | TrueLane ✅ | ⭐⭐⭐⭐⭐ | AARP members, comprehensive full-service needs |

| USAA | $950–$1,250 | ⭐⭐⭐⭐⭐ | SafePilot ✅ | ⭐⭐⭐⭐⭐ | Military veterans & qualifying family only |

| GEICO | $1,050–$1,400 | ⭐⭐⭐ | DriveEasy ✅ | ⭐⭐⭐⭐ | Budget-focused seniors, straightforward coverage |

| Travelers | $1,100–$1,500 | ⭐⭐⭐⭐ | IntelliDrive ✅ | ⭐⭐⭐⭐ | Bundle-focused seniors, IntelliDrive UBI users |

| Progressive | $1,150–$1,600 | ⭐⭐⭐ | Snapshot ✅ | ⭐⭐⭐ | Snapshot UBI power users, online-first shoppers |

| State Farm | $1,200–$1,650 | ⭐⭐⭐ | Drive Safe & Save ✅ | ⭐⭐⭐⭐ | Seniors who prefer a local agent relationship |

*Estimated 2026 national averages for a single senior driver with a clean record, standard vehicle, full coverage. Your actual rate will differ based on state, ZIP code, vehicle, and history.

How Does The Hartford (AARP) Actually Compare for Senior Drivers in 2026?

Let me be direct: The Hartford’s AARP auto program is the most thoughtfully designed insurance product for seniors on the market right now. It’s not just a discount — it’s a program built from the ground up around what older drivers actually need.

The AARP membership unlocks exclusive pricing that’s genuinely competitive — often 10–15% below what non-AARP senior drivers find elsewhere. And the program adds benefits that other carriers simply don’t match:

- Lifetime Renewability Guarantee — The Hartford won’t drop you as a customer due to age alone (some insurers quietly begin non-renewing older drivers). As long as you meet basic eligibility criteria, you can stay.

- RecoverCare — After a covered accident, this benefit covers the cost of daily household tasks you can’t perform during recovery: grocery delivery, lawn care, housecleaning. It’s a benefit genuinely designed for senior life circumstances.

- 12-Month Rate Lock — Your premium won’t increase during your policy term, even if you have an at-fault accident (with some conditions).

- TrueLane Telematics — Their UBI program rewards low-mileage, calm driving patterns — exactly what most senior drivers demonstrate.

🧍 Real Observation: Helen, 74, Pennsylvania

Helen had been with Nationwide for nine years when she came to me frustrated about a small rate increase. She was an AARP member but had never gotten a quote through The Hartford’s program. Her Nationwide rate: $1,690/year. Her Hartford AARP quote: $1,190/year — with RecoverCare included and a TrueLane enrollment that was projected to save another $140. She switched the same week.

If you’re 50 or older and not yet an AARP member, join for $16 today and get a Hartford quote this week. If you’re already an AARP member and haven’t compared Hartford rates recently, do it at your next renewal. For most non-military senior drivers, this is the first call I’d make.

Is USAA, GEICO or Travelers Cheaper for Drivers Over 65 in 2026?

USAA — The Best Rates on the Market (If You Qualify)

USAA is not available to everyone — you must be a current or former military service member, or an immediate family member of one. If you qualify, get a quote before reading another word. USAA consistently posts the lowest average rates in most states, often 10–25% below comparable carriers, combined with claims satisfaction scores that are consistently at the top of every industry survey.

Their SafePilot telematics program is well-designed and rewards calm, local driving with meaningful discounts. For senior veterans and their spouses, USAA is almost always the answer.

GEICO — Competitive Base Rates, Lighter on Senior-Specific Features

GEICO’s strength is its competitive base pricing and the DriveEasy telematics app, which can add significant savings for senior drivers with calm habits. Their weakness, in my experience, is the thinner menu of senior-specific discounts and benefits compared to The Hartford. If you want the lowest possible base rate and are comfortable managing your policy primarily online, GEICO is a strong contender — especially if you’re not an AARP member or don’t qualify for USAA.

Travelers — The Bundle and UBI Sweet Spot

Travelers earns its place in senior conversations primarily through two strengths: a strong multi-policy bundle discount and the IntelliDrive telematics program. For seniors who also own their home and want to simplify their insurance into one provider, Travelers bundles are frequently among the most competitive available. If you’re enrolling in a UBI program and also bundling, Travelers should be on your quote list.

| Carrier | Qualify for USAA? | AARP Member? | Want Bundle? | My Recommendation |

|---|---|---|---|---|

| USAA | ✅ Yes | Either | Either | Start here, full stop. |

| The Hartford (AARP) | ❌ No | ✅ Yes | Either | Best overall for most non-military seniors. |

| Travelers | ❌ No | Either | ✅ Yes | Strong for bundlers and IntelliDrive UBI users. |

| GEICO | ❌ No | Either | No preference | Good budget option; compare carefully against Hartford. |

Can You Still Get Senior Discounts If You Have a Past Accident on Your Record?

Yes — and this is an important nuance that many seniors get wrong. Having one at-fault accident on your record (especially if it’s 2+ years old) does not disqualify you from most senior discount programs. The discounts that remain fully available include:

- Mature driver / defensive driving course discount

- Low-mileage or annual mileage update

- Multi-policy bundle discount

- Vehicle safety feature discounts

- Pay-in-full and paperless discounts

Telematics programs (UBI) are also still available post-accident — and are actually one of the best tools for rebuilding your rate. If you enroll in a UBI program and demonstrate a consistent pattern of calm, low-mileage driving for 6–12 months, many carriers will factor that behavioral data into your rate at your next renewal, partially offsetting the accident surcharge.

The biggest impact of a past accident is on the base rate, not on discount eligibility. The strategy is to claim every discount available to you to offset that higher base rate as much as possible — and to get a fresh quote from at least two competitors, because accident surcharge amounts vary significantly between carriers.

Every 12 months — minimum. Set a recurring calendar reminder 6–8 weeks before your renewal date. That window gives you time to collect at least 3–4 competitive quotes, evaluate the options, and make a switch without any lapse in coverage. Loyalty rarely pays in insurance: many carriers offer their best rates to new customers, and long-standing customers often pay a “loyalty tax” of 10–20% above market rate without realizing it.

How Do You Compare Car Insurance Companies Effectively as a Senior in 2026?

Getting quotes is easy. Getting comparable quotes is the part most people mess up. Here’s the correct way to do it:

- Start with your current declarations page. Note your exact coverage levels — liability limits, deductibles, comprehensive and collision — before you start collecting quotes. You need to compare apples to apples.

- Collect at minimum 4 quotes: USAA (if eligible), The Hartford/AARP, GEICO, and one other (Travelers or State Farm based on your situation).

- Input identical coverage levels for every quote. Varying deductibles or liability limits will make comparison impossible.

- Ask each carrier specifically about senior discounts during the quote process: “What senior discounts would apply to my profile?” The numbers you get without asking are often not the best numbers available.

- Ask about telematics enrollment discounts separately: “If I enroll in your UBI program, what’s the typical discount for a driver with my profile?”

- Get every quote in writing (email or printed PDF) before making any decision. Don’t switch based on a verbal quote that might change when they run your full record.

- Factor in non-price elements: mobile app quality, local agent availability, claims satisfaction ratings, and any senior-specific features like RecoverCare.

I’ve done this comparison process dozens of times with senior drivers, and the pattern is remarkably consistent: the first quote they get back from their existing insurer is rarely their best option. The second and third quotes — especially when they proactively ask about senior discounts — almost always tell a different story. Spend 90 minutes shopping this year. It’s one of the most reliable ways to put $200–$500 back in your pocket with zero lifestyle change.

Questions Seniors Ask Most When Comparing Insurance Companies

Choose Smarter — Not Just Cheaper

The best car insurance company for you isn’t the one with the lowest advertised rate — it’s the one that offers the best total value for your specific profile, with the discounts you actually qualify for applied correctly. Before choosing any company, make sure you understand the complete breakdown of what’s available to senior drivers in 2026:

Read the complete breakdown in our pillar guide — it covers every strategy, every discount, and the specific trick that senior drivers are using to save $400–$900/year right now:

The One Car Insurance Trick Most Seniors Don’t Know About in 2026 →