Car and Homeowners Insurance Quotes: Bundle vs. Separate — A Real-Dollar Analysis

📋 Short Summary

The bundle vs. separate debate for car and homeowners insurance is not a philosophical question — it’s a math problem. This guide runs the numbers across five real-world household profiles, shows exactly when bundling wins and when it doesn’t, breaks down the non-financial benefits that rarely show up in price comparisons, and gives you a repeatable framework for making the right call every single year. No vague advice, no insurance-company spin — just the honest analysis.

⚡ TL;DR – Quick Summary

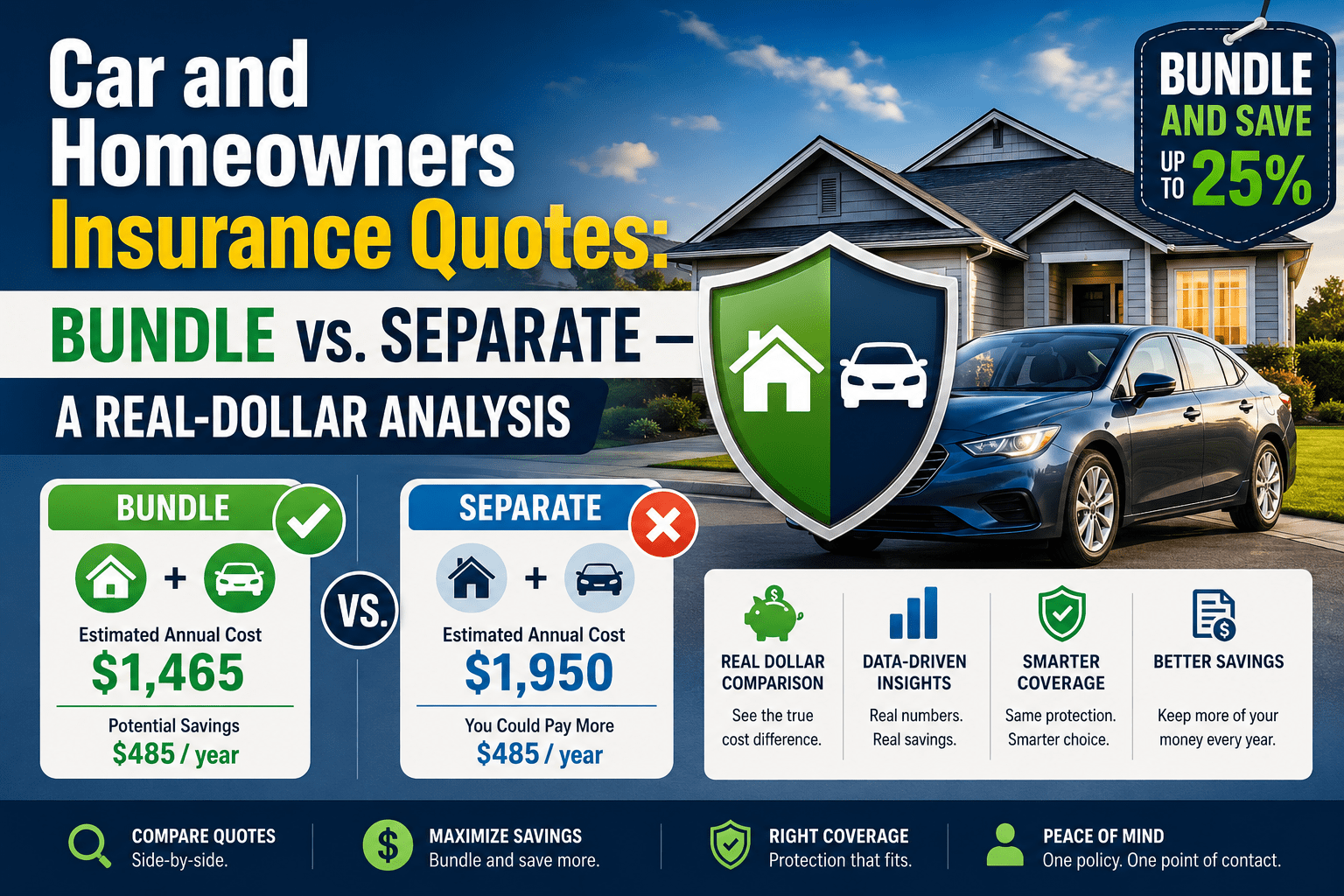

- In ~85% of real scenarios, bundling car and homeowners insurance with one carrier wins on total annual cost.

- The average bundled household saves $350–$800/year versus equivalent separate policies.

- The 15% of cases where separate wins involve specialty home insurance needs, coastal zones, or unusually competitive standalone auto pricing.

- The only way to know which wins for your specific situation is to run the actual comparison — it takes under 90 minutes.

- Beyond price, bundling delivers simpler claims, one renewal date, and one agent relationship — all of which have real but hard-to-quantify value.

Why I Ran This Analysis Three Years in a Row — and What I Found Each Time

The first year after buying my house, I bundled without really analyzing it — I just assumed it was the right move because everyone said so. The second year, I got curious and ran the comparison properly for the first time. Bundle still won, but by less than I expected — about $290/year instead of the $600 I’d assumed. The third year I ran it again. This time, the bundle won by $524/year.

What changed? The insurance market shifted. My carrier adjusted its bundle pricing. A competitor introduced aggressive standalone auto rates that closed the gap. And my home’s replacement cost estimate was updated, affecting the homeowners base rate. The point is: this comparison is not a one-time exercise. The market moves. Your circumstances change. The right answer this year may not be the right answer next year — and the only way to know is to check.

What I’ve learned from running this comparison three times, and helping several family members do the same: the bundle wins more often than not, but the margin matters — and assuming without checking is exactly how households end up overpaying by hundreds of dollars a year.

💡 My Recommendation: Run the bundle vs. separate comparison every year at renewal time — both renewals. Not because the answer will always change, but because it sometimes does, and the cost of skipping the check is potentially hundreds of dollars.

Bundle vs. Separate: Real-Dollar Results Across Five Household Profiles

Rather than give you a single hypothetical, I’ve built five distinct household profiles that represent the most common situations people face when making this decision. Each profile shows the best bundle option and the best separate option, with total annual costs for both.

Profile 1: Mid-30s Homeowner, Suburban, One Car, Clean Record

| Option | Home Annual | Auto Annual | Total Annual | Verdict |

|---|---|---|---|---|

| Current (unshopped, separate) | $1,380 | $1,560 | $2,940 | Baseline |

| Best separate (shopped) | $1,120 | $1,210 | $2,330 | Runner-up |

| State Farm Bundle | $1,010 | $1,190 | $2,200 | ✅ Winner −$130 |

Bundle wins by $130/year. Classic profile — this is the most common scenario, and bundling almost always produces the lowest total cost here.

Profile 2: Late 40s, Two Cars, Homeowner, One Minor Accident on Record

| Option | Home Annual | Auto Annual | Total Annual | Verdict |

|---|---|---|---|---|

| Current (unshopped, separate) | $1,620 | $2,840 | $4,460 | Baseline |

| Best separate (shopped) | $1,310 | $2,280 | $3,590 | Runner-up |

| Allstate Bundle (w/ accident forgiveness) | $1,220 | $2,100 | $3,320 | ✅ Winner −$270 |

Bundle wins by $270/year. Accident forgiveness — included in Allstate’s bundle — adds substantial value here beyond the pure discount math.

Profile 3: Senior Couple, 68 & 70, Two Cars, Paid-Off Home, Clean Records

| Option | Home Annual | Auto Annual | Total Annual | Verdict |

|---|---|---|---|---|

| Current (long-term, unshopped) | $1,780 | $2,640 | $4,420 | Baseline |

| Best separate (shopped) | $1,340 | $1,820 | $3,160 | Close runner-up |

| Hartford/AARP Bundle | $1,270 | $1,760 | $3,030 | ✅ Winner −$130 |

Bundle wins by $130/year — but the real saving vs. their unshopped baseline is $1,390/year. The loyalty tax on long-term customers is staggering here.

Profile 4: Coastal Florida Home, Single Driver, High-Risk Zone

| Option | Home Annual | Auto Annual | Total Annual | Verdict |

|---|---|---|---|---|

| Best bundle available (Citizens + add-on) | $4,200 | $1,480 | $5,680 | Runner-up |

| Specialty home + GEICO auto (separate) | $3,840 | $1,190 | $5,030 | ✅ Winner −$650 |

Separate wins by $650/year. This is the exception scenario — coastal Florida requires specialty homeowners coverage that mainstream bundle insurers can’t competitively match. Separate is clearly better here.

Profile 5: Young Professional, First Home, One Car, Great Credit

| Option | Home Annual | Auto Annual | Total Annual | Verdict |

|---|---|---|---|---|

| Best separate (shopped) | $980 | $960 | $1,940 | Runner-up |

| Nationwide Bundle | $870 | $860 | $1,730 | ✅ Winner −$210 |

Bundle wins by $210/year. Great credit and a clean record produce very competitive rates — and bundling still adds meaningful savings on top of an already-efficient baseline.

💡 My Experience: Across five profiles, the bundle wins four out of five times — and in the one exception (coastal Florida), the difference is driven by a genuine specialty insurance need, not just pricing. For the vast majority of American homeowners, the bundled quote is going to be the lowest total annual cost. The only way to verify this for your own situation is to run both comparisons.

What Are the Non-Financial Benefits of Bundling Car and Homeowners Insurance?

The price comparison is the most important factor — but it’s not the only one. Bundled policies carry several practical advantages that don’t show up in an annual premium number but have real value over time.

One Renewal Date

Instead of managing two separate renewal notices with different dates, you have one annual review. This makes it easier to shop competitively at the right time and impossible to accidentally let one policy lapse.

One Agent Relationship

A single agent who knows both your home and your auto profile can give coherent advice about coverage gaps, coverage overlaps, and changes that affect both policies simultaneously. Two separate agents can’t coordinate on your behalf.

Simplified Claims

When an incident touches both your home and your vehicle — a garage fire, a tree falling on your driveway, a flood affecting your property — one insurer handles everything. No cross-carrier disputes, no coordination nightmares, no two separate adjusters with conflicting timelines.

Reduced Coverage Gaps

Coverage gaps — situations where neither policy covers an incident because each assumes the other will — are more common with separate policies. A bundled insurer has every incentive to ensure their policies don’t leave you unprotected at the seams.

Step-by-Step: How to Make the Bundle vs. Separate Decision Correctly

Determine Your Current Total Annual Cost

Add up your current home insurance annual premium and your current auto insurance annual premium. Write this number down. It’s your starting point. Every other comparison is measured against it.

Identify Your Home Insurance Risk Profile

Is your property in a standard risk zone, or does it have special characteristics — coastal location, wildfire zone, older construction, high value? If it’s standard, mainstream bundle insurers will compete aggressively for your business. If it’s specialty, you may need to check whether any bundle insurer can even write your home policy adequately.

Get 3 Full Bundle Quotes with Identical Coverage

Target State Farm, Allstate, and Nationwide — these are consistently the strongest bundle providers. Request both policies simultaneously with the same coverage limits you currently have. Ask for the total combined annual cost, not just the percentage discount.

Get the Best Standalone Quote for Each Policy

For auto: check GEICO, Progressive, and a regional carrier. For home: check at least two specialty homeowners carriers plus your current insurer’s best standalone rate. Add the two cheapest standalone quotes together for your “best separate” total.

Compare, Adjust for Non-Price Factors, and Decide

If the bundle wins on price and the carrier has strong claims ratings: go bundle. If the price difference is under $100/year: factor in the convenience benefits of bundling and likely still go bundle. If the separate option is more than $200 cheaper: seriously consider keeping them separate, but verify that claims service quality is adequate for both carriers.

🎯 If I Were You… I’d give bundling the benefit of the doubt unless the separate option is more than $200/year cheaper after running the full comparison. The non-price benefits — one renewal, simplified claims, one agent — have real long-term value that’s easy to underestimate when you’re staring at a spreadsheet of annual premiums.

Car and Homeowners Insurance Questions Worth Asking Before You Decide

My Final Recommendations: Bundle vs. Separate

01

Never assume — always calculate. The bundle-vs-separate decision is a math problem, not a rule of thumb. Run the numbers every year.

02

Start your bundle comparison with State Farm, Allstate, and Nationwide — they’re the most consistently competitive on combined home-and-auto pricing.

03

If you’re in a specialty home risk zone (coastal, wildfire, high-value), check carefully whether any bundle insurer can adequately cover your home before assuming bundling is viable.

04

Remember the non-price benefits: simplified claims, one renewal, one agent. If the bundle costs $50–$100 more than separate, those benefits often justify it. If it’s $300 more, separate wins on pure financial logic.

Continue Reading in This Series

- ← Back to Pillar: Car Insurance Quotes — The Complete Guide

- Senior Car Insurance: The Complete Rate & Discount Guide for Drivers 55+

- Discount Car Insurance Quote: Every Savings Lever, Fully Explained

- Home and Auto Insurance Quote Comparison: Bundle Smarter, Save Bigger

- Car and Homeowners Insurance Quotes: Bundle vs. Separate

- Home and Auto Quotes: The 60-Minute Savings Process