Discount Car Insurance Quote: Every Savings Lever, Fully Explained

📋 Short Summary

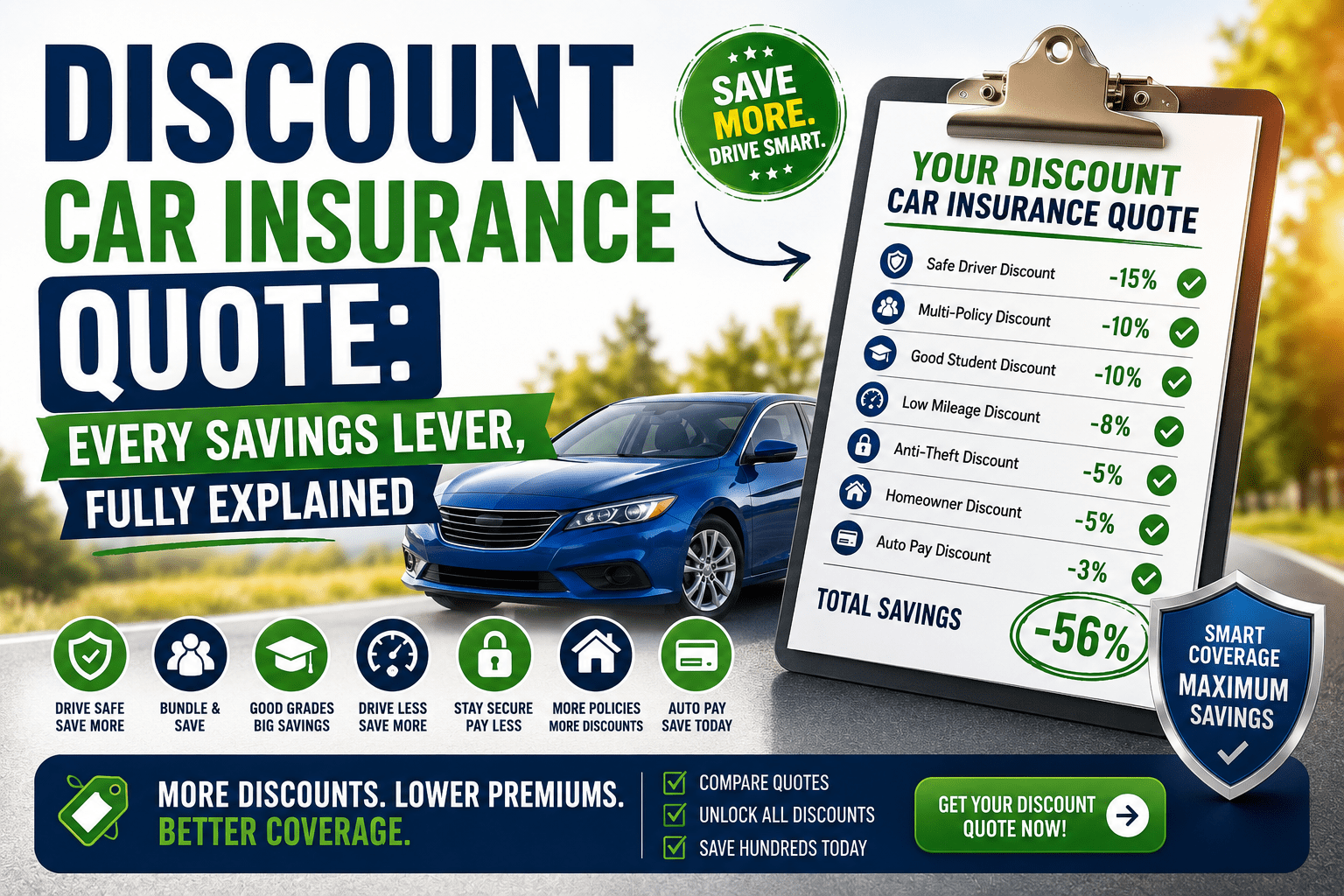

A discount car insurance quote isn’t a gimmick — it’s what your policy should look like once every applicable savings opportunity has been identified and applied. This guide breaks down every major and minor discount available to personal auto policyholders in 2026, explains exactly how to qualify for each, and shows you how to stack them systematically to reach the lowest legitimate premium your profile supports. With a real-life example, a complete discount checklist, and a comparison of which insurers offer the most generous stacking, this is the resource I wish someone had handed me years earlier.

⚡ TL;DR – Quick Summary

- The average driver qualifies for 6–10 discounts — but typically has fewer than 3 applied to their current policy.

- Stacking discounts correctly can reduce your annual premium by $300–$900+ depending on your profile.

- Discounts are almost never applied automatically — you must specifically ask for each one by name.

- The bundle discount (home + auto) is usually the single largest individual discount available.

- Telematics programs offer some of the highest discount percentages — up to 30% — for safe, low-mileage drivers.

The Phone Call That Cost Me $1,140 a Year — For Seven Years

I was on the phone with my insurer when I renewed my policy back in my early 30s. The agent walked me through the coverage, confirmed the payment, and said something I’ll never forget: “Great, and I’ve applied your good driver discount.” One discount. That was it. I said thank you and hung up.

Seven years later, when I finally sat down and compared policies seriously, I discovered I’d been missing the multi-vehicle discount (I had two cars), the paperless billing discount, the pay-in-full discount, and the homeowners discount. Each one was small individually — but together they represented about $95/month in savings I’d been hemorrhaging for nearly a decade.

$95 × 12 × 7 = $7,980. I didn’t get that money back. But I did finally stop leaving it on the table.

💡 My Recommendation: Before you finish reading this guide, pull up your current policy declarations page and check which discounts are listed. I’d be willing to bet there are at least two on this page you’re currently not receiving. The process of claiming them takes one phone call.

The Complete Discount Car Insurance Checklist: Every Discount That Exists

Print this. Bring it to every agent call. Read each line aloud and ask: “Do I qualify for this?” You will be surprised how often the answer is yes — and equally surprised how rarely the agent brought it up first.

| Discount | Typical Savings | Who Qualifies | How to Unlock | Availability |

|---|---|---|---|---|

| Multi-Policy Bundle | 15–25% | Homeowners or renters | Bundle home/renters + auto | All major |

| Good Driver | 10–22% | 3–5 yr clean record | Ask + MVR verification | All major |

| Telematics / Usage-Based | 10–30% | Safe, low-mileage drivers | Enroll in app/device program | Most major |

| Multi-Vehicle | 8–15% | 2+ vehicles in household | Insure all cars together | All major |

| Pay-in-Full (Annual) | 5–10% | All policyholders | Pay full annual premium upfront | All major |

| Paperless / Auto-Pay | 2–5% | All policyholders | Enroll in e-billing + auto-pay | All major |

| Defensive Driving Course | 5–15% | Most drivers (esp. seniors) | Complete state-approved course | Most major |

| Good Student | 5–15% | Student under 25, GPA 3.0+ | Submit transcript each term | All major |

| Student Away at School | 5–10% | Student 100+ miles from home, no car | Provide enrollment documentation | Most major |

| Anti-Theft / Safety Features | 3–8% | Anti-theft device, alarm, VIN etching | Confirm installed features | Most major |

| New Car | 5–10% | Vehicle under 3 years old | Confirm vehicle model year | Most major |

| Military / Veteran | 5–15% | Active military or veteran | Provide service verification | GEICO, USAA, others |

| Professional / Occupation | 3–10% | Teacher, nurse, government, engineer | State profession at enrollment | Select insurers |

| Loyalty / Long-Term Customer | 3–8% | 5+ years with same insurer | Often automatic — ask anyway | Most major |

| Early Signing / New Policy | 2–5% | Sign 1–2 weeks before renewal date | Don’t wait until last minute to switch | Progressive, others |

How Does Discount Stacking Actually Work — and What Does It Look Like in Real Numbers?

Discount stacking is exactly what it sounds like: applying multiple discounts simultaneously to a single policy. Not all insurers allow unlimited stacking, and the math isn’t always purely additive — but the cumulative effect is almost always dramatic.

Let me walk through a real scenario. Take a 42-year-old homeowner named Sandra — clean record, two cars, commutes 8 miles each way, and pays annually. Her baseline quote before discounts: $1,920/year. Here’s what happens when we stack:

| Discount Applied | Discount % | Running Annual Premium | Annual Savings So Far |

|---|---|---|---|

| Baseline (no discounts) | — | $1,920 | $0 |

| + Good Driver Discount | −15% | $1,632 | $288 |

| + Multi-Vehicle (2 cars) | −10% | $1,469 | $451 |

| + Bundle (home + auto) | −18% | $1,205 | $715 |

| + Pay-in-Full | −7% | $1,121 | $799 |

| + Paperless + Auto-Pay | −3% | $1,087 | $833 |

| + Telematics Enrollment | −18% | $892 | $1,028 |

| Final Premium After Stacking | −54% total | $892/yr | $1,028 saved |

*Illustrative scenario. Actual discounts are calculated differently by each insurer and may not be fully additive in all cases. Real results vary.

💡 My Experience: Sandra’s scenario is not exceptional — it’s typical for a driver who simply takes the time to ask. The difference between her $1,920 baseline and her $892 final premium isn’t magic; it’s a series of phone calls and one online enrollment. The discounts existed all along. She just needed to activate them.

Step-by-Step: How to Build Your Own Maximum-Discount Car Insurance Quote

Audit Your Current Policy for Missing Discounts

Log into your insurer’s portal and find your discount summary — usually under “Policy Details” or “My Discounts.” Cross-reference this with the full checklist above. Any discount on the list that isn’t on your policy is a potential savings opportunity. Mark each gap.

Prepare Your “Discount Qualification Evidence” Before Calling

For good driver: know your MVR is clean. For good student: have a recent transcript. For defensive driving: have your completion certificate. For anti-theft: know what devices your car has. Agents apply discounts faster and more reliably when you have evidence ready during the call.

Call Your Current Insurer and Read the Discount List

Start with your existing insurer — this is your baseline. Read each discount on the checklist and ask specifically: “Am I currently receiving this discount, and do I qualify?” Note every discount that gets applied. Then ask: “Is there anything else I haven’t mentioned that might reduce my rate?” This second question is where hidden savings often live.

Repeat the Process with 3–4 Competing Insurers

Different insurers have different discount structures and weight individual discounts differently. A discount worth 8% at one carrier might be worth 15% at another. An independent agent who shops multiple carriers simultaneously is invaluable here — they can run this comparison in a single conversation.

Enroll in Telematics on Your Winning Policy

Once you’ve chosen your best base quote, enroll in the insurer’s telematics program. Most programs give you an enrollment discount immediately, before they’ve even seen your driving data. For safe drivers, the eventual behavior-based discount is one of the most substantial ongoing savings available.

Schedule Annual Discount Reviews

Life changes unlock new discounts. A child turning 16 (adds a driver — shop multi-vehicle discounts). A child heading to college (student-away discount). A retirement (low-mileage discount). Marriage (often reduces rates). Getting a mortgage (homeowner bundle discount). Any of these life events should trigger a discount review.

Which Insurers Offer the Best Discount Programs — and How Do They Compare?

| Insurer | Discount Count | Best Single Discount | Telematics Max | Stacking Flexibility |

|---|---|---|---|---|

| Progressive | 13+ | Multi-policy (up to 20%) | 30% (Snapshot) | ⭐⭐⭐⭐⭐ |

| State Farm | 10+ | Multi-policy (up to 17%) | 30% (DSS) | ⭐⭐⭐⭐ |

| GEICO | 16+ | Multi-vehicle (up to 25%) | 25% (DriveEasy) | ⭐⭐⭐⭐⭐ |

| Allstate | 12+ | Bundle (up to 25%) | 25% (Drivewise) | ⭐⭐⭐⭐ |

| Nationwide | 11+ | Vanishing deductible program | 40% (SmartRide) | ⭐⭐⭐⭐ |

🎯 If I Were You… I’d specifically check Nationwide’s SmartRide program if you’re a safe driver. A potential 40% discount on your driving behavior alone is the highest ceiling in the mainstream market. Even if you don’t ultimately stay with Nationwide, use that number as leverage when negotiating with other carriers.

Questions About Car Insurance Discounts That People Rarely Think to Ask

My Final Recommendations: How to Get the Most Discount-Stacked Quote Possible

01

Print the full discount checklist and read it aloud to every agent you speak to. Agents don’t volunteer discounts proactively. You have to drive that conversation.

02

Always compare fully-discounted final quotes — not base rates. A higher base rate with more discounts often ends up cheaper than a low base rate with few discounts.

03

Enroll in telematics on every policy where you drive safely and predictably. It’s the highest-percentage individual discount in the market for well-qualified drivers.

04

Calendar-track every discount expiry date. Rate creep from expired discounts is silent, automatic, and entirely preventable.

Continue Reading in This Series

- ← Back to Pillar: Car Insurance Quotes — The Complete Guide

- Senior Car Insurance: The Complete Rate & Discount Guide for Drivers 55+

- Discount Car Insurance Quote: Every Savings Lever, Fully Explained

- Home and Auto Insurance Quote Comparison: Bundle Smarter, Save Bigger

- Car and Homeowners Insurance Quotes: Bundle vs. Separate

- Home and Auto Quotes: The 60-Minute Savings Process