Car Insurance Quotes: Everything You Need to Know to Stop Overpaying

📋 Short Summary

Car insurance quotes are not created equal — and most people settle for the first number they see. This guide breaks down every major quote category: auto insurance, cheap car insurance, senior rates, discount bundles, and home-and-auto combo packages. You’ll walk away with a clear strategy, a comparison framework, and the exact questions I use every single year when I re-shop my own coverage. Whether you’re 25 or 75, a homeowner or a renter, driving a brand-new SUV or a 12-year-old sedan — there is a smarter, cheaper policy waiting for you. You just have to know how to find it.

⚡ TL;DR – Quick Summary

- The average American overpays by $400–$700/year simply by never shopping around.

- Bundling your home and auto insurance can slash your combined premium by 15–25%.

- Seniors qualify for exclusive discounts most agents never proactively mention.

- Getting at least 3–5 quotes before signing anything is the single highest-ROI move you can make.

- Cheap doesn’t mean bad — it often means you finally asked the right questions.

Why I Started Caring About Car Insurance Quotes (And Why You Should Too)

A few years back, I was paying $187 a month for car insurance. My car was a seven-year-old Honda Accord with 94,000 miles on it. No accidents, no tickets, nothing. I assumed that was just… the going rate. My agent had been with me for years, I trusted him, and I never asked questions.

Then my neighbor — same zip code, similar car, clean record — mentioned she was paying $109 a month. I almost choked on my coffee. That’s nearly $940 a year that I was leaving on the table. For no reason. That weekend, I sat down and started comparing car insurance quotes for the first time in six years. By Monday morning, I had a new policy at $114/month with better coverage.

That experience changed how I think about insurance entirely. It’s not a fixed cost. It’s a negotiable expense — if you know the rules.

💡 My Recommendation #1: Set a calendar reminder every 12 months to re-shop your car insurance quotes. Loyalty to one insurer is costing most Americans hundreds of dollars a year. The market changes. Your life changes. Your rate should too.

What Exactly Is a Car Insurance Quote — and How Is It Calculated?

A car insurance quote is an estimate — sometimes surprisingly accurate, sometimes wildly off — of what you’ll pay monthly or annually for a given level of coverage. It’s generated by feeding your personal data into an insurer’s underwriting algorithm, which weighs dozens of risk factors simultaneously.

The critical thing to understand is that every insurer uses a different algorithm. Two companies looking at the exact same driver can produce quotes that differ by $80 a month. Not because one is better — but because their models weight your risk profile differently. This is why comparing matters so much.

What Factors Are Secretly Driving Your Quote Up (or Down)?

| Rating Factor | Impact Level | Can You Control It? | Typical Premium Swing |

|---|---|---|---|

| Driving record (tickets/accidents) | Very High | ✅ Yes (time + behavior) | +20% to +80% |

| Credit score | Very High | ✅ Yes (long-term) | +15% to +50% |

| ZIP code / location | High | ⚠️ Rarely | +10% to +40% |

| Vehicle make / model / age | High | ✅ Yes (choice of car) | +10% to +35% |

| Annual mileage | Medium | ✅ Yes | +5% to +20% |

| Marital status / homeownership | Medium | ⚠️ Partially | −5% to −15% |

| Coverage level (deductible, limits) | Very High | ✅ Yes (your choice) | −10% to −40% |

| Multi-policy bundle discount | High Savings | ✅ Yes | −15% to −25% |

Looking at that table, you’ll notice something important: most of the factors that raise your premium are ones you can actually influence over time. The ones you can’t control — like your ZIP code — are often offset by the ones you can.

Auto Insurance Quotes vs. Car Insurance Quotes: Is There Actually a Difference?

Technically, no. The terms are used interchangeably across the industry. “Auto insurance” tends to be the more formal, industry-standard term, while “car insurance” is what most people say out loud. When you’re searching for quotes online, you’ll see both — and they’ll lead you to the same products.

That said, “auto” can sometimes encompass motorcycles, RVs, and commercial vehicles, while “car insurance” is usually understood to mean personal passenger vehicles. For the purposes of this guide, I’m using them interchangeably — we’re talking about insuring the vehicle you drive every day.

What Types of Coverage Are Inside a Typical Auto Insurance Quote?

Liability Coverage

Covers damage you cause to others. Required by law in most states. This is the floor — not the ceiling.

Collision Coverage

Pays to repair your own car after an accident — regardless of fault. Usually comes with a deductible.

Comprehensive Coverage

Covers non-collision damage: theft, fire, weather, animals. Often overlooked — and often more affordable than people expect.

Uninsured Motorist

Protects you when the at-fault driver has no insurance. About 1 in 8 drivers is uninsured. This coverage is worth every cent.

PIP / MedPay

Covers medical expenses for you and passengers regardless of fault. Required in no-fault states. A smart add-on everywhere else.

Roadside Assistance / Rental

Add-ons that cost very little but can be lifesavers. I never skip these — a tow truck call alone can cost $150+.

How Do You Actually Get the Best Car Insurance Quote? My Step-by-Step Process

I’ve done this process three times in the last eight years — each time saving at least $600 annually. Here’s exactly what I do, in order. No fluff.

Gather Your Information Before You Start

Before visiting any quote tool, have the following ready: your driver’s license number, VIN for every vehicle, current coverage details, annual mileage estimate, and your credit score (rough range is fine). Being prepared speeds everything up and gives you more accurate quotes.

Decide on Your Coverage Level First

Don’t just accept the default quote. Choose your deductible ($500 vs $1,000 vs $2,000), decide if you need collision and comprehensive (especially for older cars), and think about whether you need gap insurance if you’re financing. Knowing what you want before you start comparing prevents apples-to-oranges comparisons.

Get at Least 5 Quotes from Different Sources

Don’t stop at two or three. Use a mix of: one national direct insurer (like GEICO, Progressive, or State Farm), one regional insurer, one independent agent who shops multiple carriers, and one aggregator site. The variance is often shocking.

Ask Specifically About Every Discount Available

Good drivers discount, multi-car discount, home and auto bundle, paperless billing, pay-in-full, student away at school, anti-theft device, military/veteran, low-mileage. These are rarely applied automatically. You must ask. Every. Single. Time.

Compare Apples to Apples — Then Negotiate

Once you have 5 quotes with identical coverage levels, rank them. Then call your top two choices and ask: “Is this your best rate? I have a competing offer at $X.” I’ve had insurers drop their rate on the spot by $18–22/month doing exactly this. Never feel awkward about it.

Read the Policy — Especially the Exclusions

Before you sign, spend 15 minutes on the declarations page and the exclusions section. Know what’s not covered. I once found that my “comprehensive” policy excluded flood damage in my specific flood-risk area. Worth knowing before you need it.

Is Cheap Car Insurance Actually Worth It — or a Trap?

Let me be direct: cheap car insurance is not automatically bad insurance. The word “cheap” has a PR problem. What you actually want is optimal value — the best coverage for the price you’re paying. Sometimes that’s the most affordable option on the market. Sometimes it’s not.

The genuine danger of cheap car insurance lies in hidden gaps in coverage — low liability limits, suspiciously high deductibles, or stripped-out comprehensive protection. Those gaps are invisible until you file a claim. And by then, it’s too late.

Cheap Car Insurance: Smart Strategies vs. Warning Signs

| Strategy / Sign | ✅ Smart Savings | ⚠️ Red Flag |

|---|---|---|

| Higher deductible ($1,500–$2,000) | ✅ | — |

| Dropping collision on a 12+ year old car | ✅ | — |

| Paying annually instead of monthly | ✅ | — |

| Minimum state liability limits only | — | ⚠️ |

| No uninsured motorist coverage | — | ⚠️ |

| Insurer with D or F customer service rating | — | ⚠️ |

| Telematics / usage-based discount program | ✅ | — |

🎯 If I Were You… I’d raise my deductible to $1,000 or $1,500 and put the monthly savings into a dedicated “car emergency” savings account. In most cases, you’ll never need to touch it — but if you do, it’s there. This is the single smartest way to self-insure the gap while still being protected against catastrophic losses.

For a deep dive into finding the lowest legitimate rates without sacrificing real protection, read my dedicated guide: How to Find Genuinely Cheap Car Insurance Without Getting Burned.

What Every Senior Driver Needs to Know About Car Insurance Rates

Here’s something that doesn’t get talked about enough: your 60s are often the cheapest years of your insurance life. Decades of safe driving, a clean record, and a reliable vehicle can all combine to produce rock-bottom premiums. My father-in-law was shocked when he re-shopped at 67 and found his rate dropped $42/month compared to when he was 54.

The challenge usually begins around age 75–80, when insurers start pricing in statistically higher claim rates for older drivers. But even then, senior-specific discounts can offset a significant portion of any rate increase — if you know to ask for them.

For the full breakdown on rates, discounts, and the unique coverage needs of drivers 55+, see our dedicated guide: Senior Car Insurance: How to Get the Best Rates After 55.

How Do Discount Car Insurance Quotes Work — and Which Ones Are Worth Chasing?

The term “discount car insurance quote” sounds like marketing — and sometimes it is. But many real, stackable discounts exist inside every major policy. The problem is that they’re not automatically applied. You have to know what to ask for.

I keep a running list that I read aloud to every new agent I speak to. By the end of the call, I’ve usually unlocked at least 3–4 discounts I wasn’t getting before. The average savings from stacking legitimate discounts is $200–$500 per year per vehicle.

| Discount Type | Typical Savings | Who Qualifies | How to Claim |

|---|---|---|---|

| Multi-policy / Bundle | 15–25% | Homeowners/renters | Bundle with same insurer |

| Good Driver | 10–20% | 3–5 year clean record | Ask + verify record |

| Defensive Driving Course | 5–15% | Most drivers (esp. seniors) | Complete approved course |

| Pay in Full (Annual) | 5–10% | All policyholders | Pay full premium upfront |

| Telematics / Snapshot | 10–30% | Safe/low-mileage drivers | Install app or device |

| Multi-Vehicle | 8–15% | 2+ cars in household | Insure all vehicles together |

| Paperless / Auto-Pay | 2–5% | All policyholders | Enroll in e-billing |

Want the full breakdown with real examples and a discount checklist you can print and bring to your next call? Read: The Complete Discount Car Insurance Quote Guide: Every Savings Lever, Explained.

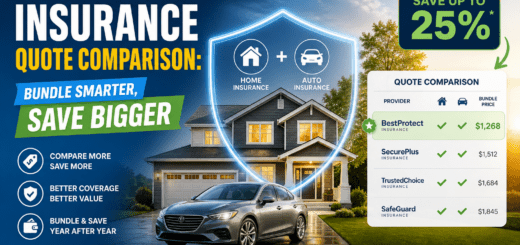

Why Is Home and Auto Insurance Quote Comparison the Smartest Financial Move Most Homeowners Skip?

If you own a home and a car — and you don’t have them insured with the same company — there’s a very real chance you’re overpaying by $300–$800 per year. The home-and-auto bundle is consistently one of the highest-value discounts in the insurance world, and it’s available to virtually everyone who qualifies for both policies.

The savings come from two directions at once: you get a multi-policy discount on your auto premium and a matching discount on your homeowners premium. Both drop simultaneously. When I bundled my policies three years ago, my car insurance dropped by $21/month and my home insurance dropped by $18/month — a combined annual saving of $468 for about 45 minutes of comparison shopping.

For a full comparison of the top bundling options and a real-dollar breakdown, see: Home and Auto Insurance Quote Comparison: How to Bundle Smartly and Save Big.

Car and Homeowners Insurance Quotes: When Does Bundling Make the Most Sense?

Bundling isn’t always the right answer for everyone — and any agent who tells you otherwise is selling, not advising. There are situations where keeping policies separate — with different best-in-class providers — actually saves more money than bundling. But those cases are the exception, not the rule.

The key is comparing the bundle price against the sum of your best standalone quotes. That comparison takes about an hour and can produce real, meaningful savings. Our full breakdown lives here: Car and Homeowners Insurance Quotes: Bundle vs. Separate — A Side-by-Side Analysis.

How to Get the Most Accurate Home and Auto Quotes in Under an Hour

The single biggest mistake people make when getting home and auto quotes together is letting the process drag out over days or weeks. I’ve done this in under 60 minutes — including both policies — and consistently gotten competitive results.

The secret is having everything organized before you start: your home’s square footage, year built, roof age, claims history, current deductibles, and replacement cost estimate. Have your vehicle info ready at the same time. Feed both sets of data to 3–4 insurers simultaneously, and you’ll have comparable bundle quotes on your desk before dinner.

See the full workflow guide here: Home and Auto Quotes: The 60-Minute Process That Could Save You $500+ This Year.

How Do the Major Car Insurance Providers Actually Compare?

I’ve personally gotten quotes from all of the major national insurers at least twice. Here’s my honest, side-by-side read on them — balanced for price, claims handling, discounts, and bundling capability.

| Insurer | Best For | Avg. Price vs. Market | Bundle Available | Claims Rating | Senior Discounts |

|---|---|---|---|---|---|

| State Farm | Agents + service | Slightly Above | ✅ Strong | ⭐⭐⭐⭐⭐ | ✅ Yes |

| GEICO | Low base price | Below Avg. | ⚠️ Limited | ⭐⭐⭐⭐ | ✅ Yes |

| Progressive | Price comparison tool | Competitive | ✅ Yes | ⭐⭐⭐½ | ✅ Yes |

| Allstate | Bundling / features | Above Avg. | ✅ Strong | ⭐⭐⭐ | ✅ Yes |

| USAA | Military families | Well Below Avg. | ✅ Excellent | ⭐⭐⭐⭐⭐ | ✅ Yes |

| Nationwide | Vanishing deductible | Slightly Above | ✅ Yes | ⭐⭐⭐⭐ | ✅ Yes |

💡 My Experience: I’ve found GEICO to be the consistent price leader for clean-record drivers in suburban areas. But their bundling options are weaker than State Farm or Allstate — so if you own a home, the overall cheapest solution is often NOT GEICO. Run the full bundle math before deciding.

Questions Nobody Asks (But Everyone Should)

My Final Recommendations: What I Would Do If I Were Starting From Zero

01

Get a minimum of 5 quotes — not 2, not 3. The spread between quote #1 and quote #5 is almost always surprising.

02

If you own a home: always run the bundle math. The combined savings on both policies usually exceeds any individual-policy advantage.

03

Ask about every discount — literally read the list aloud. Agents don’t volunteer this information.

04

Re-shop every 12 months, even if you’re happy. Happiness fades fast when you realize you’ve been paying 20% more than your neighbor.

Keep Reading: Deep-Dive Guides in This Series

Discount Car Insurance Quote: Every Savings Lever, Fully Explained

Home and Auto Insurance Quote Comparison: Bundle Smarter, Save Bigger

Car and Homeowners Insurance Quotes: Bundle vs. Separate — A Real-Dollar Analysis

Home and Auto Quotes: The 60-Minute Process That Could Save You $500+ This Year

2 Responses

[…] ← Back to Pillar: Car Insurance Quotes — The Complete Guide […]

[…] ← Back to Pillar: Car Insurance Quotes — The Complete Guide […]